51A125 Kentucky PDF Template

51A125 Kentucky PDF Template

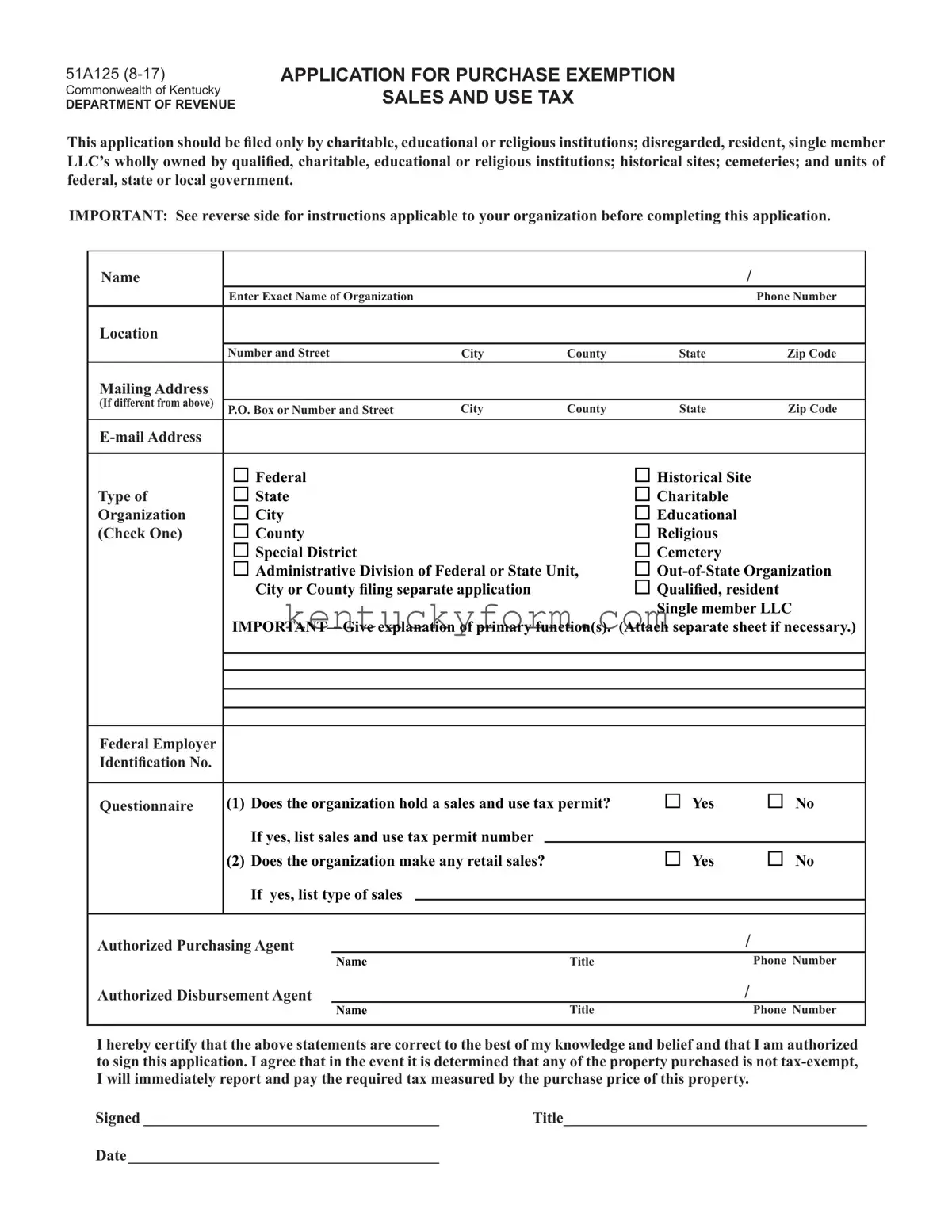

In the Commonwealth of Kentucky, the Department of Revenue provides a means for specific organizations to request an exemption from sales and use tax through the 51A125 form. This particular form is designed solely for use by entities operating within charitable, educational, or religious sectors, alongside other specified organizations such as historical sites, cemeteries, and various government units. The application process necessitates a detailed disclosure of the organization's primary functions, alongside requisite documentation that substantiates their eligibility for tax exemption. These documents include, but are not limited to, Articles of Incorporation, financial records, and letters of determination from the IRS or relevant heritage commissions. Upon successful application, organizations are granted the ability to make qualifying purchases without the added financial burden of sales tax, provided these purchases serve the organization's tax-exempt functions. Significantly, the form accentuates the importance of maintaining updated records with the Department of Revenue, ensuring any changes in the organization's operational scope or status are accurately reflected. As such, the 51A125 form represents a critical tool for eligible organizations, allowing them to allocate resources more efficiently in service of their exempt purposes, while complying with Kentucky's regulatory framework.

51A125

Commonwealth of Kentucky

DEPARTMENT OF REVENUE

APPLICATION FOR PURCHASE EXEMPTION

SALES AND USE TAX

This application should be filed only by charitable, educational or religious institutions; disregarded, resident, single member LLC’s wholly owned by qualified, charitable, educational or religious institutions; historical sites; cemeteries; and units of federal, state or local government.

IMPORTANT: See reverse side for instructions applicable to your organization before completing this application.

Name |

|

|

|

|

|

/ |

|

|

|

Enter Exact Name of Organization |

|

|

|

|

Phone Number |

||

Location |

|

|

|

|

|

|

|

|

|

Number and Street |

City |

County |

State |

Zip Code |

|||

Mailing Address |

|

|

|

|

|

|

|

|

(If different from above) |

|

|

|

|

|

|

|

|

P.O. Box or Number and Street |

City |

County |

State |

Zip Code |

||||

|

||||||||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Federal |

|

|

|

Historical Site |

|

||

Type of |

State |

|

|

|

Charitable |

|

||

Organization |

City |

|

|

|

Educational |

|

||

(Check One) |

County |

|

|

|

Religious |

|

||

|

Special District |

|

|

|

Cemetery |

|

||

|

Administrative Division of Federal or State Unit, |

|

||||||

|

City or County filing separate application |

|

Qualified, resident |

|||||

|

|

|

|

|

|

Single member LLC |

||

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Federal Employer |

|

|

|

|

|

|

|

|

Identification No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Questionnaire |

(1) Does the organization hold a sales and use tax permit? |

Yes |

No |

|||||

|

If yes, list sales and use tax permit number |

|

|

|

|

|||

|

(2) Does the organization make any retail sales? |

|

Yes |

No |

||||

|

If yes, list type of sales |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Authorized Purchasing Agent |

|

|

|

/ |

|

|||

|

|

Name |

|

|

Title |

|

Phone Number |

|

Authorized Disbursement Agent |

|

|

|

/ |

|

|||

|

|

Name |

|

|

Title |

|

Phone Number |

|

|

|

|

|

|

|

|

|

|

I hereby certify that the above statements are correct to the best of my knowledge and belief and that I am authorized to sign this application. I agree that in the event it is determined that any of the property purchased is not

Signed ______________________________________ |

Title_______________________________________ |

Date________________________________________

SPECIAL INSTRUCTIONS

Charitable, Educational and Religious Institutions and Qualified, Resident Single Member LLC’s

(1)A copy of the Articles of Incorporation;

(2)detailed schedule of receipts and disbursements must be attached to this application.

(3)The letter from the Internal Revenue Service which determines that your organization is exempt from income taxation under Section 501(C)(3) of the Internal Revenue Code must be attached to this application.

Historical Sites

(1)A copy of the letter from the Kentucky Heritage Commission confirming your listing in the National Register must be attached to this application.

(2)Admission charges to historical sites qualifying for exemption are not subject to sales tax. However, historical sites are liable for tax on any other retail sales such as meals, arts and crafts, souvenirs, etc.

Units of Federal, State or Local Government

(1)Units of local government include cities, counties and all special districts as defined in KRS 65.005.

(2)Special districts must attach a copy of the registration filed with the county clerk as required by KRS 65.005.

(3)Each administrative division within a federal or state unit, city or county which performs a specific function and makes purchases in its own name is required to file a separate application.

Cemeteries

(1)A copy of the Articles of Incorporation and a detailed schedule of receipts and disbursements must be attached to this application.

(2)Attach a copy of the ruling which grants the organization an exemption from property tax.

IF YOUR APPLICATION IS APPROVED

(1)You will be permitted to make purchases of tangible personal property, digital property or services without payment of sales and use tax to the supplier. However, purchases of any items not to be used within the exempt function of the organization are taxable.

(2)Aletter of authorization will be mailed to you which will contain an exemption number and instructions for properly claiming the exemption on purchases.

(3)If the organization makes taxable sales and is not an educational or charitable institution, a sales and use tax permit is required.

In addition to the above, you must submit a copy of the exemption letter or authorization to show proof of exemption from sales tax in your state.

IMPORTANT: The Department of Revenue must be notified promptly of any change in the name, address or nature of the organization

from the information submitted in this application. Please refer to the purchase exemption number issued to the organization when corresponding with the Department.

Mail completed application to the Kentucky Department of Revenue, Division of Sales and Use Tax, P.O. Box 181, Station 67, Frankfort, Kentucky,

| Fact Name | Description |

|---|---|

| Form Number and Title | 51A125 - Application for Purchase Exemption Sales and Use Tax |

| Issuing Body | Commonwealth of Kentucky Department of Revenue |

| Applicant Eligibility | Charitable, educational, religious institutions, single member LLCs owned by qualifying institutions, historical sites, cemeteries, and government units |

| Governing Law | Kentucky Revised Statutes (KRS) and Section 501(C)(3) of the Internal Revenue Code for tax-exempt status |

| Primary Purpose | To apply for an exemption from sales and use tax for eligible purchases |

| Application Requirements | Incorporation articles, financial schedules, IRS exemption letter, and, if applicable, proof of historical registration or local government registration |

| Exemption Use | For purchases of tangible personal property, digital property, or services used within the organization's exempt function |

| Exemption Limitations | Items not used within the exempt function are taxable |

| Authorization Documentation | A letter of authorization containing an exemption number and purchase exemption instructions |

| Special Instructions for Various Entities | Detailed for charitable, educational, religious institutions, historical sites, government units, and cemeters according to their specific needs |

| Notification Requirement for Changes | Organizations must promptly notify the Department of Revenue of any changes in name, address, or organizational nature |

Once the decision has been made to apply for a Purchase Exemption for Sales and Use Tax in Kentucky, the 51A125 form needs to be completed accurately to ensure a smooth submission process. This application is crucial for charitable, educational, religious institutions, and other specified organizations seeking exemption from sales and use tax on qualifying purchases. The form includes essential information about the organization, its activities, and authorization by an official representative. Special instructions based on the organization's type are provided to guide the attachment of necessary documentation. Following these steps carefully will ensure that the application is thorough and leads to a successful exemption claim.

Upon submitting the 51A125 form, the application will be processed for approval. Successful organizations will receive a letter of authorization containing an exemption number and further instructions on applying the exemption to eligible purchases. It is important to keep the Department of Revenue updated with any changes to the organization's information to maintain the exemption status. This careful attention to detail and compliance will facilitate the exemption process, allowing the organization to focus more on its primary functions and less on tax liabilities.

What is the purpose of the 51A125 Kentucky form?

The 51A125 Kentucky form is an application designed for charitable, educational, or religious institutions, along with other specified organizations such as disregarded entities, single member LLCs fully owned by qualified institutions, historical sites, cemeteries, and various government units. Its primary purpose is to apply for a sales and use tax purchase exemption, allowing these entities to make purchases without paying the sales and use tax, provided those purchases are for use within their exempt functions.

Who can file a 51A125 Kentucky form?

Eligible entities include charitable, educational, and religious institutions; disregarded, resident, single member LLCs wholly owned by qualified charitable, educational, or religious institutions; historical sites; cemeteries; and units of federal, state, or local government. Each organization must meet specific criteria and provide necessary documentation to qualify for the exemption.

Does an organization need a sales and use tax permit to apply for the exemption?

No, holding a sales and use tax permit is not a prerequisite for applying for the exemption using the 51A125 form. However, the form does inquire whether the organization already possesses such a permit, indicating that both permit holders and non-holders can apply, depending on their qualification for the exemption.

What information is required to complete the 51A125 form?

Organizations need to provide their name, contact information, the federal employer identification number, and details about their primary functions. Additionally, the form requires information about authorized purchasing and disbursing agents, an explanation of the organization's exempt functions, and whether it makes retail sales. Specific supporting documents are also needed based on the nature of the institution applying.

What documentation must accompany the 51A125 form?

Depending on the type of organization, different documents are required. For charitable, educational, and religious institutions, copies of the Articles of Incorporation, a detailed financial record, and a letter from the IRS confirming tax-exempt status are needed. Historical sites must attach a letter from the Kentucky Heritage Commission. Units of government and special districts have additional requirements, such as registration with a county clerk. Cemeteries need to include their Articles of Incorporation and evidence of exemption from property tax.

What happens after the application is approved?

Upon approval, the organization will receive a letter of authorization containing an exemption number and guidance on claiming the exemption when making eligible purchases. This permits the organization to buy tangible personal property, digital property, or services without paying the sales and use tax, as long as the items are used within the exempt functions of the organization.

Are there any taxable purchases for organizations with the exemption?

Yes, purchases not used within the exempt functions of the organization remain taxable. This includes any items or services purchased by the organization that do not directly relate to its charitable, educational, or religious activities and missions.

Is the exemption applicable to out-of-state organizations?

Out-of-state organizations can apply for the exemption but must submit additional proof of exemption from sales tax in their state. This ensures that only entities recognized as exempt in their home jurisdiction can benefit from Kentucky's exemption.

What if my organization undergoes changes after receiving the exemption?

The Kentucky Department of Revenue must be notified promptly of any changes in the name, address, or nature of the organization from what was submitted in the application. This ensures that the exemption remains valid and applicable to the organization's current operations and structure.

Where should the completed 51A125 form be submitted?

The completed application, along with all required documentation, should be mailed to the Kentucky Department of Revenue, Division of Sales and Use Tax, at the address provided on the form. This ensures proper processing and review of the application for the sales and use tax purchase exemption.

When filling out the 51A125 Kentucky Purchase Exemption Sales and Use Tax application, many individuals and organizations encounter common errors that can delay or affect approval. Understanding these mistakes is crucial for ensuring a smooth application process.

To ensure a successful application process, applicants should carefully review the special instructions applicable to their organization type, such as Charitable, Educational and Religious Institutions; Historical Sites; Units of Federal, State or Local Government; and Cemeteries. These instructions detail the specific documentation that must be attached to the application. For example, historical sites must include a copy of the letter from the Kentucky Heritage Commission, while government units are required to attach registration filed with the county clerk. Understanding and adhering to these instructions can dramatically improve the likelihood of application approval.

In summary, a thorough and attentive approach when completing the 51A125 Kentucky form is essential. By avoiding these common errors and ensuring all required documentation is attached, organizations can navigate the application process more efficiently. This not only helps in obtaining the necessary exemption status but also facilitates compliance with state tax regulations.

When you're dealing with the 51A125 Kentucky form, it's crucial to gather all necessary documents to ensure a smooth application process. This form, essential for charitable, educational, or religious institutions seeking a sales and use tax purchase exemption, often requires supplementary documentation to support your application. Understanding these additional forms and documents can greatly assist in navigating the complexities of tax exemption applications.

Collecting these documents is a step towards ensuring that your application for purchase exemption under the 51A125 Kentucky form is complete and accurate. Each document plays a critical role in painting a full picture of your organization’s operations, financial integrity, and eligibility for tax exemption. It’s advisable to review each requirement carefully and prepare your documentation well in advance to avoid any delays or obstacles in your application process. Remember, the goal is to facilitate a seamless application procedure, allowing your organization to benefit from the tax exemptions it rightfully qualifies for.

The 51A125 Kentucky form shares similarities with the Texas Sales and Use Tax Exemption Certification. Both documents serve organizations seeking exemption from sales and use tax, specifically catering to entities like charitable, educational, or religious institutions. While the Kentucky form requires detailed information about the organization, including its primary function and attachments like Articles of Incorporation, the Texas equivalent also mandates information that demonstrates the organization's eligibility for tax exemption. Both forms function as a pivotal step for eligible organizations to conduct their activities without bearing the standard sales and use tax, underscoring the importance of clear and pertinent documentation to support their tax-exempt status.

Similar to the Streamlined Sales and Use Tax Agreement (SSUTA) Exemption Certificate, the 51A125 form facilitates tax exemption for qualifying purchases made by eligible entities. The SSUTA Exemption Certificate, used by multiple states, standardizes the process for claiming sales tax exemptions across participating states. Likewise, the 51A125 Kentucky form aims to streamline the exemption process within Kentucky for specific organizations. Both documents necessitate thorough validation of the organization’s eligibility for tax-exempt purchases, ensuring that the exemptions are granted to entities that genuinely qualify under the law, thus highlighting the role of regulatory measures in maintaining the integrity of tax exemption procedures.

The California Resale Certificate shares a foundational objective with the 51A125 Kentucky form: both enable organizations to acquire goods or services without the immediate imposition of sales tax, emphasizing the use of such items within the organization's exempt operations. In California, resellers acquire this certificate to purchase items for resale without sales tax, contingent upon the resale of the purchased items. The 51a125 form allows for a similar exemption but is tailored towards the operational purchases of charitable, historical, or educational institutions, among others. Despite their diverse geographical and functional contexts, both forms pivot on the necessity of detailed and accurate documentation to substantiate the tax exemption claim.

The New York State ST-119.1 Exempt Organization Certificate represents a similar tool to the 51A125 form in the array of documents designed to validate an organization's tax exemption status. Aimed at non-profit organizations within New York, the ST-119.1 certificate necessitates comprehensive information to demonstrate eligibility for tax-exempt purchases, mirroring the Kentucky form’s requirements for a detailed account of the organization's nature and function. Both states implement these forms to carefully vet organizations, ensuring that only those entities that strictly comply with the criteria for exemption can benefit from the statute. This selective scrutiny underscores the efforts by states to ensure that tax exemptions serve their intended purpose of supporting eligible non-profit and charitable endeavors.

Successfully completing the 51A125 Kentucky form, a crucial document for organizations seeking a purchase exemption for sales and use tax, requires attention to detail and a clear understanding of the process. Here are essential dos and don'ts that can guide you through accurately filling out the application:

Do:

Don't:

Understanding the Kentucky 51A125 form can sometimes be confusing, leading to common misconceptions. It's imperative to demystify these to ensure organizations can accurately apply for the purchase exemption sales and use tax without any hiccups. Here are eight misconceptions about the 51A125 Kentucky form:

Correcting these misconceptions ensures that qualifying organizations can smoothly navigate the application process, fully understand their obligations and the scope of their exemptions, and adhere to Kentucky's tax laws. Awareness and comprehension of these misconceptions are critical for all parties involved in the exemption application process.

Filling out and using the 51A125 Kentucky form is an essential process for certain organizations seeking a purchase exemption on sales and use tax. Understanding the form’s requirements can help ensure that your application is complete and processed efficiently. Here are some key takeaways to guide you through this process:

Remember, this form is integral for organizations that qualify to make tax-exempt purchases for their operational use. Properly completing and submitting the 51A125 with the necessary documentation helps in availing of this benefit without any hassle. Paying attention to the details and the special instructions for your specific organization type will aid in a smoother process.

If your organization conducts any taxable sales outside the scope of educational or charitable activities, be prepared to apply for a sales and use tax permit as required. This ensures that all facets of your organization's operations remain in compliance with Kentucky tax laws.

Aoc Ru 004 - Provides the specific address and communication channels for submitting record request forms.

Kentucky Ev Incentives - A non-refundable fee, paid to the Kentucky State Treasurer, is required, with amounts varying by license type and renewal status.

Khsaa Physical Form 2023 - For cheerleading and dance participants, physical exams must be submitted by a specified deadline before tryouts.