741 Kentucky PDF Template

741 Kentucky PDF Template

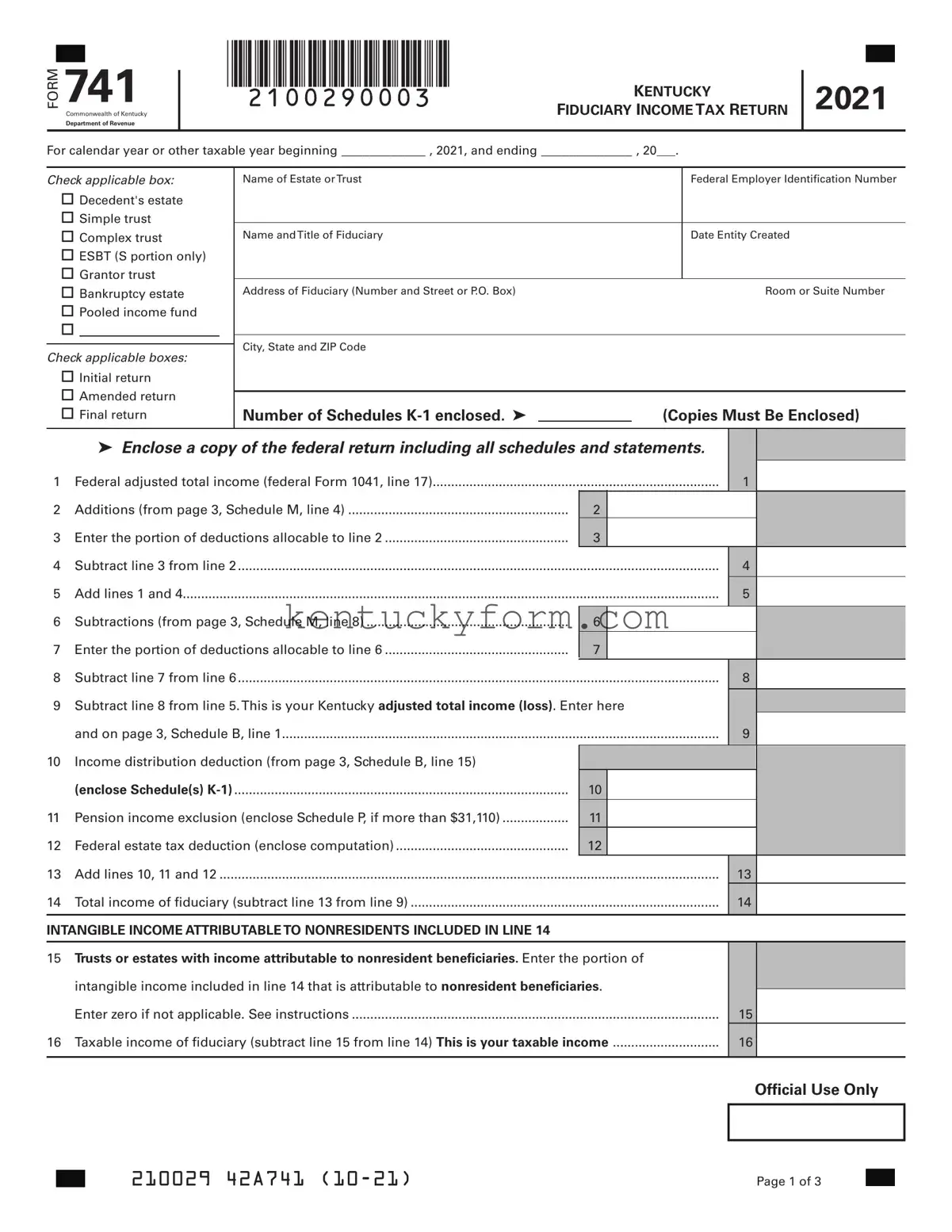

The Form 741, known as the Kentucky Fiduciary Income Tax Return, plays a critical role for estates and trusts within Kentucky. This form is utilized to report the income, deductions, and income tax liability of estates and trusts for a given tax year, highlighting the fiscal responsibilities these entities have to the state. Whether the entity is a decedent's estate, a simple, complex, or grantor trust, or a bankruptcy estate, Form 741 ensures the proper accounting of income and allocations relevant to such entities for the year 2005. It mandates the inclusion of a Federal Employer Identification Number, details about the fiduciary, and the tax period it covers. Several checkboxes provide for different statuses of the return, indicating if it's an initial, amended, or final return while outlining the obligations for attaching schedules, including Schedule K-1 for income distributions and other relevant federal return documents. The form intricately details additions and subtractions to federal adjusted income, ties to federal estate tax deductions, pensions, and specifies tax computations alongside credits. For entities with nonresident beneficiaries, it addresses the allocation of intangible income, rounding off with the declaration section to be signed under the penalties of perjury, affirming the accuracy of the provided information. With sections dedicated to charitable deductions, income distribution deductions, and detailed schedules for adjustments to income, Form 741 provides a comprehensive framework for fiduciary entities to comply with Kentucky's income tax requirements.

741

Commonwealth of Kentucky

Department of Revenue

KENTUCKY

FIDUCIARY INCOME TAX RETURN

2021

For calendar year or other taxable year beginning ____________ , 2021, and ending _____________ , 20___.

Check applicable box:

Decedent's estate

Simple trust

Complex trust

ESBT (S portion only)

Grantor trust

Bankruptcy estate

Pooled income fund

Check applicable boxes:

Initial return

Amended return

Final return

Name of Estate or Trust |

Federal Employer Identification Number |

|

|

Name and Title of Fiduciary |

Date Entity Created |

|

|

Address of Fiduciary (Number and Street or P.O. Box) |

Room or Suite Number |

|

|

City, State and ZIP Code |

|

Number of Schedules |

|

(Copies Must Be Enclosed) |

|

Enclose a copy of the federal return including all schedules and statements. |

|

1 |

Federal adjusted total income (federal Form 1041, line 17) |

1 |

2 |

Additions (from page 3, Schedule M, line 4) |

2 |

3 |

Enter the portion of deductions allocable to line 2 |

3 |

4 |

Subtract line 3 from line 2 |

4 |

5 |

Add lines 1 and 4 |

5 |

6 |

Subtractions (from page 3, Schedule M, line 8) |

6 |

7 |

Enter the portion of deductions allocable to line 6 |

7 |

8 |

Subtract line 7 from line 6 |

8 |

9 |

Subtract line 8 from line 5. This is your Kentucky adjusted total income (loss). Enter here |

|

|

and on page 3, Schedule B, line 1 |

9 |

10 |

Income distribution deduction (from page 3, Schedule B, line 15) |

|

|

(enclose Schedule(s) |

10 |

11 |

Pension income exclusion (enclose Schedule P, if more than $31,110) |

11 |

12 |

Federal estate tax deduction (enclose computation) |

12 |

13 |

Add lines 10, 11 and 12 |

13 |

14 |

Total income of fiduciary (subtract line 13 from line 9) |

14 |

INTANGIBLE INCOME ATTRIBUTABLE TO NONRESIDENTS INCLUDED IN LINE 14

15Trusts or estates with income attributable to nonresident beneficiaries. Enter the portion of intangible income included in line 14 that is attributable to nonresident beneficiaries.

Enter zero if not applicable. See instructions |

15 |

16 Taxable income of fiduciary (subtract line 15 from line 14) This is your taxable income |

16 |

Official Use Only

210029 42A741 |

Page 1 of 3 |

FORM 741 (2021)

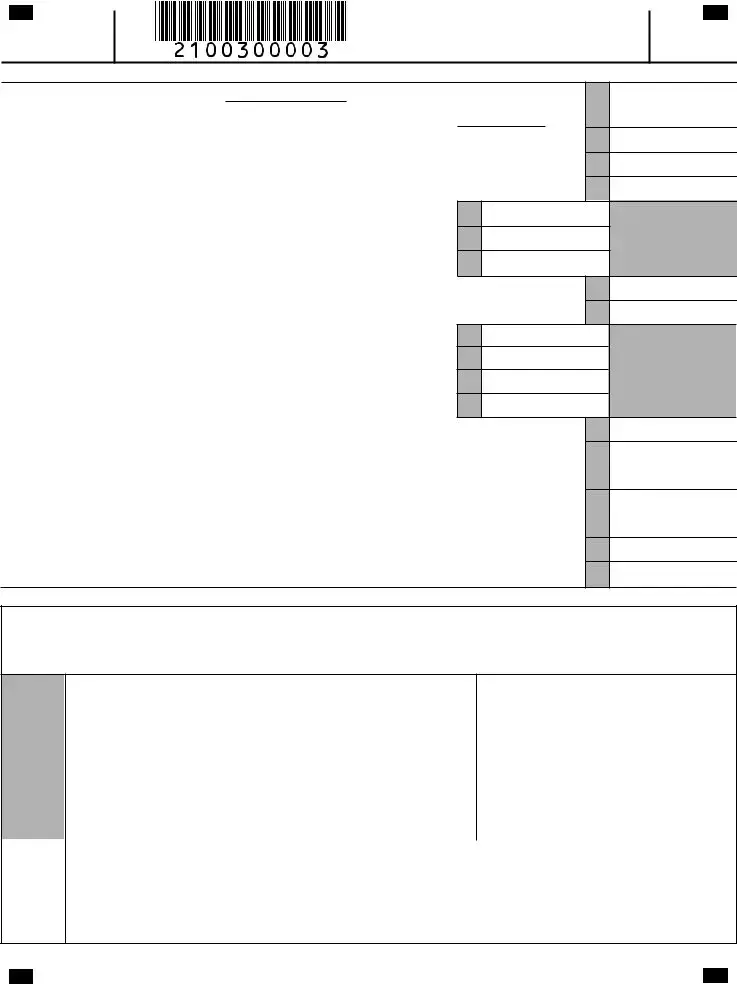

Page 2 of 3

TAX COMPUTATION |

|

|

|

||

17 |

(a) |

Tax: multiply line 16 by 5% (.05) |

and add tax from: |

|

|

|

(b) |

Form |

Total |

17c |

|

18 |

Nonrefundable credit(s) (specify and enclose supporting documents) |

18 |

|||

19 Enter Tax Credit ($2 for a trust; $10 for an estate). This credit is not refundable |

19 |

||||

20 |

Total Tax (subtract lines 18 and 19 from line 17(c); if line 18 plus line 19 is more than line 17(c), enter |

20 |

|||

21 |

(a) |

Estimated tax/Extension payments |

21a |

|

|

|

(b) |

Withholding |

21b |

|

|

|

(c) |

Nonresident Withholding from Form |

21c |

|

|

|

(d) |

Total of amounts on line 21(a) through 21(c) |

|

21d |

|

22 |

If line 20 is larger than line 21(d), subtract line 21(d) from line 20, and enter the TAX DUE |

22 |

|||

23 |

(a) |

Estimated tax penalty Check if Form |

23a |

|

|

|

(b) |

Interest |

23b |

|

|

|

(c) |

Late payment penalty |

23c |

|

|

|

(d) |

Late filing penalty |

23d |

|

|

24 |

Add lines 23(a) through 23(d) |

|

24 |

||

25 |

If the total of lines 20 and 24 is more than line 21(d), subtract line 21(d) from the total of lines 20 and |

|

|||

|

24. This is the AMOUNT YOU OWE |

|

25 |

||

26 |

If line 21(d) is more than the total of lines 20 and 24, subtract lines 20 and 24 from line 21(d). This is |

|

|||

|

the AMOUNT YOU OVERPAID |

|

26 |

||

27 |

Amount of line 26 to be CREDITED TO YOUR 2022 ESTIMATED TAX |

27 |

|||

28 |

Subtract line 27 from line 26. This is the amount to be REFUNDED TO YOU |

28 |

|||

I declare under the penalties of perjury that this return (including any accompanying schedules and statements) has been examined by me and, to the best of my knowledge and belief, is a true, correct and complete return.

Signature of Fiduciary or Agent |

Date |

Sign |

|

|

|

|

Here |

PTIN or Identification Number of Fiduciary or Agent |

|

Telephone Number (daytime) |

|

|

|

|

|

|

|

Signature of Preparer |

|

Date |

|

Paid |

|

|

|

|

Name of Preparer or Firm |

|

ID Number |

||

Preparer |

|

|||

|

|

|

||

Use |

|

|

|

|

Telephone No. |

May the DOR discuss this return with this preparer? |

|||

|

||||

|

|

|

¨ Yes ¨ No |

|

|

|

|

|

|

Mail To: |

Kentucky Department of Revenue |

|

|

|

Frankfort, KY |

|

|

||

|

|

|

||

|

|

|

|

|

|

Check Payable: Kentucky State Treasurer |

|

|

|

Payment |

|

|

||

|

Include: Your FEIN and “KY Income |

|

||

|

|

|

|

|

210030 42A741

FORM 741 (2021)

Page 3 of 3

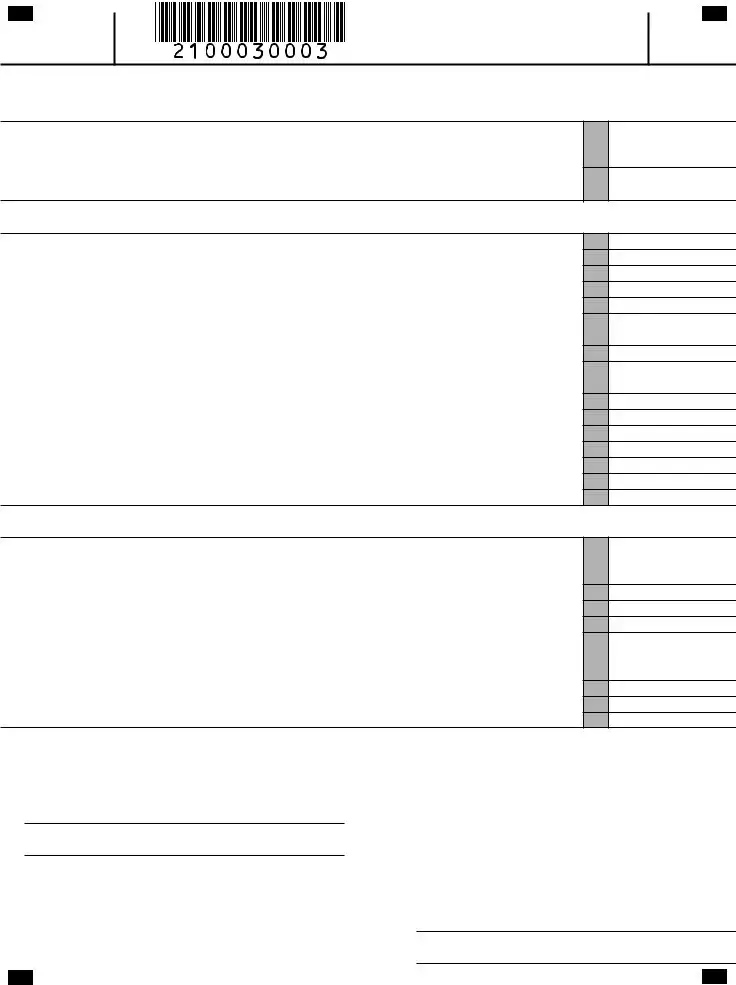

SCHEDULE

Complete Schedule A only if you made additions to or subtractions from total income on page 1, lines 2 or 6 and claimed a charitable deduction on federal Form 1041.

1Kentucky taxable income that was paid or set aside for charitable purposes and was not reported on federal Form 1041, Schedule A, including additional capital gains. Enter here and include on Schedule M, line 7 ...............................................................................................................................................................

2Kentucky

1

2

SCHEDULE

1 |

Adjusted total income (enter amount from page 1, line 9) |

1 |

2 |

Adjusted |

2 |

3 |

Net gain shown on Schedule D, Form 741, column 1, line 19 (if net loss, enter zero) |

3 |

4 |

Enter amount included from federal Schedule A, line 4 |

4 |

5 |

Enter net capital gains included on Kentucky Schedule A, line 1 or line 2 |

5 |

6Enter any Kentucky gains included on page 1, line 9 as a negative figure. If capital loss, enter as a

positive figure. (Kentucky gain/loss includes federal figures plus Kentucky adjustments.) |

6 |

7 Distributable net income (combine lines 1 through 6) |

7 |

8If complex trust, enter accounting income for tax years as determined under the governing

|

instrument and applicable law |

8 |

9 |

Amount of income required to be distributed currently |

9 |

10 |

Other amounts paid, credited or otherwise required to be distributed |

10 |

11 |

Total distributions (add lines 9 and 10) (If greater than line 8, see federal instructions.) |

11 |

12 |

Enter the amount of |

12 |

13 |

Tentative income distribution deduction (subtract line 12 from line 11) |

13 |

14 |

Tentative income distribution deduction (subtract line 2 from line 7) |

14 |

15 |

Income distribution deduction (enter the smaller of line 13 or line 14 here and on page 1, line 10) |

15 |

SCHEDULE M (FORM 741)

Part

1 Enter interest from bonds issued by other states and their political subdivisions .......................................

2 Enter additions from partnerships, fiduciaries and S corporations (enclose schedule) ...............................

3 Other additions (enclose schedule) ...................................................................................................................

4 Total additions. Enter here and on page 1, line 2 .............................................................................................

Part

5 Enter interest from U.S. government obligations (enclose schedule)............................................................

6 Enter subtractions from partnerships, fiduciaries and S corporations (enclose schedule) ..........................

7 Other subtractions (enclose schedule) ..............................................................................................................

8 Total subtractions. Enter here and on page 1, line 6........................................................................................

1

2

3

4

5

6

7

8

ADDITIONAL INFORMATION REQUIRED

1Was a Kentucky fiduciary income tax return filed for 2020? Yes No. If "No," state reason.

2If the fiduciary has income not taxed by Kentucky, have you deducted only that portion of expenses allocable to taxable income? Yes No. If "Yes," enclose computation.

3Did the estate or trust have any passive activity loss(es)? Yes No. (If "Yes," enter the loss(es) on Form

210003 42A741

4If a federal audit changed the taxable income as originally reported for any prior year, a copy of the Revenue Agent’s Report must be submitted to the Department of Revenue. Do not attach to this return.

5During the taxable year did you make an accumulation distribution as defined in Sec. 665(b), Internal Revenue Code? Yes No. If "Yes," enclose federal Schedule J (Form 1041).

6If this is an amended return, check the appropriate box on page 1. Explain changes below. Enclose a separate page if necessary.

| Fact Number | Description |

|---|---|

| 1 | The Form 741 is a Kentucky Fiduciary Income Tax Return, used for reporting income for estates and trusts. |

| 2 | This form is applicable for both calendar year and other taxable year filings, specified by the beginning and ending dates within the taxation year 2005. |

| 3 | Form 741 caters to different types of fiduciary entities including decedent's estates, simple trusts, complex trusts, grantor trusts, and bankruptcy estates. |

| 4 | Fiduciaries are required to attach a copy of the federal return along with all schedules and statements when submitting Form 741. |

| 5 | The calculation of Kentucky adjusted total income involves additions and subtractions to the federal adjusted total income, as indicated through a series of steps on the form. |

| 6 | An income distribution deduction is available and must be calculated as part of the tax return process. This is accompanied by a necessity to attach Schedule K-1. |

| 7 | Form 741 requires detailed information regarding intangible income attributable to nonresidents, affecting the taxable income of fiduciaries. |

| 8 | The tax computation section includes calculations for nonrefundable credits, specific tax credits ($2 for a trust; $20 for an estate), and outlines the procedure for determining the total tax and payments due. |

| 9 | Governed by Kentucky state law, this form is crucial for compliance with state tax obligations for fiduciaries, ensuring that estates and trusts are taxed accordingly within Kentucky. |

Filling out the Form 741, also known as the Kentucky Fiduciary Income Tax Return, is a task that requires attention to detail. This document is crucial for those managing an estate or trust in Kentucky, ensuring compliance with state tax regulations. Following a clear step-by-step guide can make the process smoother and help avoid common mistakes. Once the form is accurately filled out and submitted, the focus shifts to handling any potential tax liabilities or refunds, making it an essential step for fiduciaries managing financial responsibilities for estates or trusts.

Completing Form 741 with careful attention ensures that the fiduciary responsibilities are met with compliance to Kentucky's tax laws. This systematically organized approach aids in a thorough execution of tax filing duties for estates and trusts, ultimately safeguarding fiduciary adherence to state requirements.

What is Form 741 Kentucky?

Form 741, known as the Kentucky Fiduciary Income Tax Return, is a document used by estates or trusts to report income, deductions, gains, losses, and taxes due to the state of Kentucky. It applies to various types of fiduciary entities including decedent's estates, simple trusts, complex trusts, grantor trusts, and bankruptcy estates for a specific tax year.

Who needs to file Form 741?

Any fiduciary entity like an estate or trust that has taxable income in Kentucky or is administered in Kentucky is required to file Form 741. This includes entities that have generated income within the state, those responsible for entities with Kentucky ties, and cases where the fiduciary has a filing requirement due to financial activities within the state.

What information is needed to complete Form 741?

To accurately fill out Form 741, you'll need the federal employer identification number of the estate or trust, information about the fiduciary, the entity's federal adjusted total income, and details about any income attributable to nonresident beneficiaries. Additionally, copies of the federal return including all schedules and statements, any necessary Kentucky schedules, and documentation for credits or deductions claimed are necessary.

How do amendments to Form 741 work?

If there's a need to correct or update information previously submitted on Form 741, you can file an amended return. To do this, clearly mark the amended return box on page 1, provide the corrected information, and attach an explanation of the changes. It's also recommended to attach a separate page if the explanation does not fit in the provided space.

What are Schedule M and Schedule B in Form 741?

Schedule M (Form 741) deals with additions to and subtractions from federal adjusted total income. It includes sections for reporting interest from other states, adjustments from partnerships or S corporations, and other taxable income modifications specific to Kentucky.

Schedule B pertains to the income distribution deduction. It's used to calculate adjusted total income, distributable net income, and ultimately the income distribution deduction, which factors into the fiduciary's total income on the tax return.

When is Form 741 due?

The due date for filing Form 741 aligns with the federal tax return deadline for fiduciaries, which is typically on April 15th for calendar year filers. If the estate or trust operates on a fiscal year, the return is due on the 15th day of the fourth month following the end of their taxable year. It's important to note that extensions for filing do not extend the due date for any tax payments due.

Filling out tax forms can often be a daunting task, especially for those who are not familiar with the specific requirements and details needed. The Kentucky Form 741, designated for fiduciary income tax returns, is no exception. Errors in this form can delay processing times, trigger audits, or even result in the imposition of penalties. Let's explore the ten common mistakes individuals often make while completing this form:

While these errors are common, they can be avoided with careful attention to the details of the form and its instructions. Individuals tasked with completing the Kentucky Form 741 should take extra care in reviewing their entries and the required documentation before submission. Additionally, seeking assistance from a tax professional when uncertainty arises can be invaluable in ensuring the accuracy and completeness of the fiduciary income tax return.

Understanding these common mistakes can empower fiduciaries and agents to accurately prepare the Form 741 and help streamline the process, ensuring compliance with Kentucky's tax laws and reducing the likelihood of encountering issues with the Kentucky Department of Revenue.

When completing the Form 741 Kentucky Fiduciary Income Tax Return, several additional forms and documents may be required to provide a comprehensive overview of an estate or trust's financial status. Understanding each is crucial for ensuring compliance and accuracy in tax reporting.

Ensuring that all relevant forms and documents are completed and attached to Form 741 is vital for the accurate and legal reporting of fiduciary income within Kentucky. Each document plays a crucial role in painting a complete financial picture and adhering to both federal and state tax regulations.

The 741 Kentucky Fiduciary Income Tax Return is closely related to the Federal Form 1041, U.S. Income Tax Return for Estates and Trusts. Both documents are used to report income, deductions, and gains or losses managed by fiduciaries on behalf of an estate or trust. They require similar information, such as the entity's identification number, the fiduciary's name and address, and a detailed accounting of the income distributions made during the tax year. However, while Federal Form 1041 applies to filings across the United States, the 741 form is specifically tailored to meet Kentucky's state tax requirements.

Another document resembling Form 741 is the Schedule K-1, which details the share of income, deductions, and credits allocated to beneficiaries of trusts or estates. While the Schedule K-1 provides individual breakdowns to beneficiaries about their respective portions, Form 741 compiles the overall fiduciary activities to be reported to the Kentucky Department of Revenue. The connection lies in the need to attach copies of Schedule K-1 to the Form 741 to ensure the amounts reported at both the entity and individual beneficiary levels are consistent.

The Federal Schedule D (Form 1041), Capital Gains and Losses, is similar to parts of Form 741 that deal with reporting capital gains or losses from the estate or trust. Both documents are essential for accurately capturing the financial activities related to investments held by the entity. They ensure that any capital gains or losses impacting the fiduciary’s taxable income are correctly reported to the tax authorities, albeit one focuses on federal tax implications and the other on Kentucky state tax requisites.

Form 4972-K, Kentucky Tax on Lump-Sum Distributions, shares similarities with Form 741 in the context of how specific types of income are taxed under Kentucky law. When an estate or trust receives a lump-sum distribution that qualifies for special tax treatment, the details of this distribution and its tax calculation would influence the information reported on Form 741. Both forms contribute to the delineation of specialized income categories and their respective tax treatments within the state of Kentucky.

Schedule RC-R, Related to Credits and Incentives, also parallels the 741 form in the way it deals with reducing the tax obligation through applicable credits. While Form 741 serves as the primary document for fiduciary income reporting, the Schedule RC-R allows for the detailing of credits that the fiduciary might be eligible for, thus directly impacting the final tax calculated on Form 741. This demonstrates the interconnectedness of Kentucky’s tax forms in optimizing an estate or trust’s tax liabilities.

Schedule M (FORM 741) strongly correlates with the main body of Form 741 since it directly supplements it with details about additions to and subtractions from federal adjusted total income to arrive at Kentucky adjusted total income. This schedule reflects the modifications necessary to reconcile the differences between federal and state taxable income, showcasing the meticulous process of state-specific income tax calculation for fiduciaries.

The Federal Estate Tax Computation form (often included in filings alongside the Federal Form 1041) is akin to the sections within Form 741 that relate to deductions like the Federal estate tax deduction. Both seek to reconcile the estate’s tax obligations across different government levels, providing mechanisms to avoid double taxation on the same income streams. While they operate within their respective tax jurisdictions, their goals align in ensuring fair and accurate tax practices are applied to estates and trusts.

Finally, the Kentucky Passive Activity Loss Limitations (Form 8582-K) relate to Form 741 through the specific treatment of passive activity losses. Similar to the nuanced treatment of different income and loss types, Form 8582-K’s results feed into the preparation of Form 741, ensuring that only the allowable losses according to Kentucky’s tax laws are applied, affecting the taxable income reported by the fiduciary. This interaction exemplifies the layered approach to handling complex fiduciary tax situations.

Filling out the 741 Kentucky Fiduciary Income Tax Return requires attention to detail to ensure accuracy and compliance with Kentucky state tax laws. Below, you'll find a list of things you should and shouldn't do when completing this form:

Things You Should Do:

Things You Shouldn't Do:

When dealing with Form 741, the Kentucky Fiduciary Income Tax Return, there are a number of common misconceptions that can lead to confusion among filers. Understanding these misconceptions is crucial for preparing an accurate and compliant tax return for estates or trusts.

By dispelling these misconceptions, fiduciaries can approach Form 741 with a clearer understanding, ensuring compliance with Kentucky tax laws and potentially reducing the tax burden on the estate or trust.

When completing and utilizing the 741 Kentucky Fiduciary Income Tax Return, there are several key points to keep in mind:

By following these guidelines carefully, preparers can ensure the 741 Kentucky Fiduciary Income Tax Return is filled out accurately and in compliance with Kentucky tax laws, facilitating a smoother tax process for estates and trusts.

How to Fill Out K-4 Form Kentucky - The document includes fields for employer identification and breaks down employee earnings by city, aiding local tax compliance.

Khsaa Physical Form 2023 - This form collects essential medical information and physical examination records for new students intending to participate in sports.