Kentucky 51A113 PDF Template

Kentucky 51A113 PDF Template

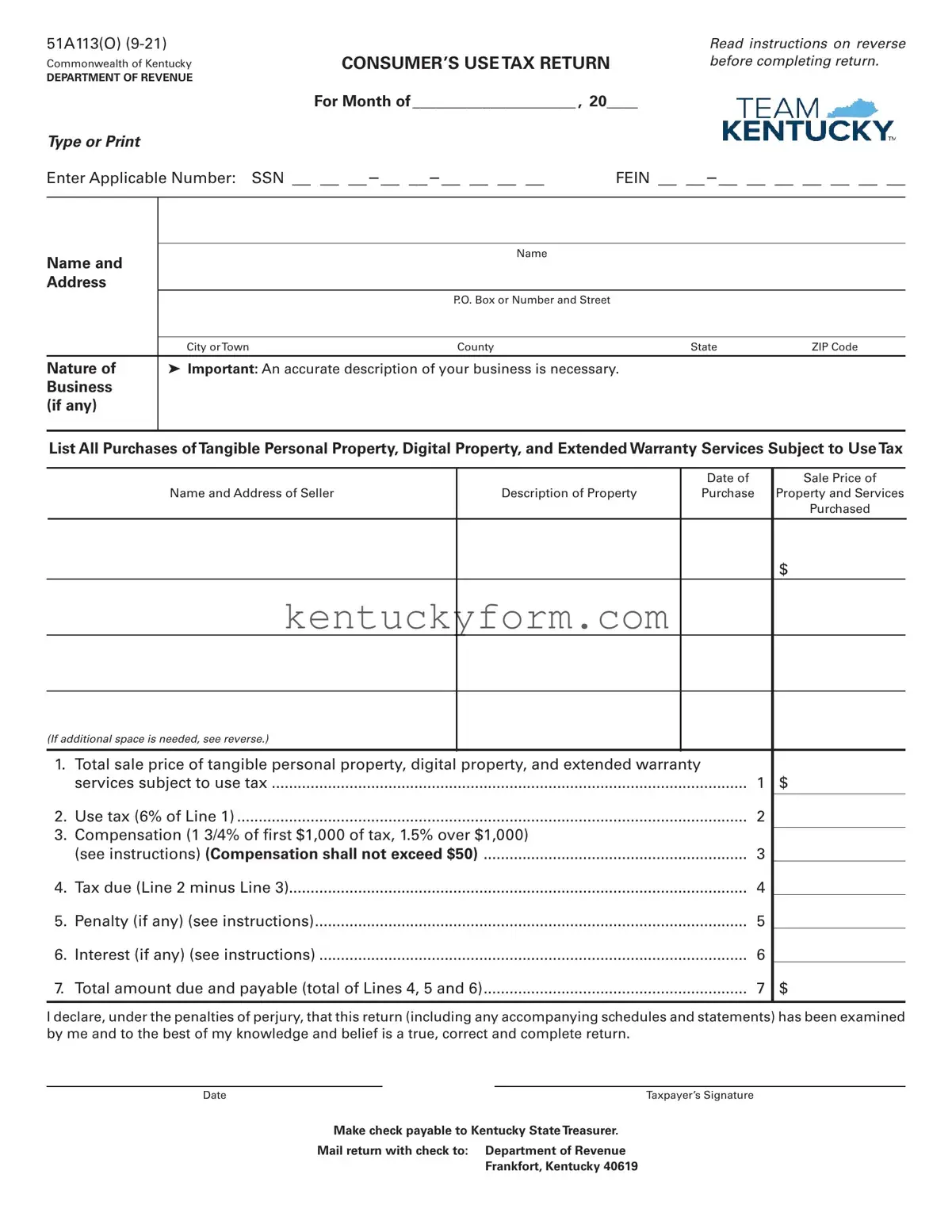

The Kentucky 51A113 form stands as a necessary document for individuals or entities in Kentucky that find themselves in the position of owing use tax on purchases. This form is dedicated to the reporting and payment of use tax on tangible personal property, digital property, and extended warranty services when Kentucky sales or use tax hasn't been paid at the time of purchase. It requires detailed listings of each taxable purchase, including the date of sale, price, and seller's information, ensuring the state's Department of Revenue can accurately assess the owed taxes. Notably, the form distinguishes between different statuses of filers, providing specific instructions for those not registered as consumers or retailers. With a tax rate set at 6 percent of the purchase price for applicable items, the form also guides taxpayers on calculating compensation, penalties, and interest due, should they apply. Designed for submission by a defined due date following the month of purchase, it includes provisions for those needing additional space to list their taxable purchases, ensuring comprehensive reporting. Remittance of payment is directed to the Kentucky State Treasurer, emphasizing the structured approach the state takes in managing use tax obligations. This necessity bridges the gap for revenue collection on purchases made without payment of Kentucky sales tax, underscoring the importance of the 51A113 form in maintaining tax compliance within the state.

51A113(O) |

|

Read instructions on reverse |

Commonwealth of Kentucky |

CONSUMER’S USE TAX RETURN |

before completing return. |

DEPARTMENT OF REVENUE |

|

|

|

For Month of _____________________ , 20____ |

|

Type or Print |

|

|

Enter Applicable Number: |

SSN __ __ __ – __ __ – __ __ __ __ |

FEIN __ __ – __ __ __ __ __ __ __ |

|

|

|

|

|

Name and |

|

Name |

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

P.O. Box or Number and Street |

|

|

|

|

|

|

|

|

City or Town |

County |

State |

ZIP Code |

|

|

|

|

|

Nature of |

Important: An accurate description of your business is necessary. |

|

|

|

Business |

|

|

|

|

(if any) |

|

|

|

|

|

|

|

|

|

List All Purchases of Tangible Personal Property, Digital Property, and Extended Warranty Services Subject to Use Tax

|

|

|

|

|

Date of |

|

Sale Price of |

|

Name and Address of Seller |

|

Description of Property |

|

Purchase |

|

Property and Services |

|

|

|

|

|

|

|

Purchased |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(If additional space is needed, see reverse.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Total sale price of tangible personal property, digital property, and extended warranty |

|

|

|

|||

|

services subject to use tax |

|

|

1 |

$ |

||

2. |

Use tax (6% of Line 1) |

|

|

2 |

|

||

|

|

|

|||||

3. |

Compensation (1 3/4% of first $1,000 of tax, 1.5% over $1,000) |

|

|

|

|||

|

|

|

|||||

|

(see instructions) (Compensation shall not exceed $50) |

............................................................. |

|

|

3 |

|

|

4. |

Tax due (Line 2 minus Line 3) |

|

|

4 |

|

||

5. |

Penalty (if any) (see instructions) |

|

|

5 |

|

||

6. |

Interest (if any) (see instructions) |

|

|

6 |

|

||

7. |

Total amount due and payable (total of Lines 4, 5 and 6) |

............................................................. |

|

|

7 |

$ |

|

|

|

|

|

|

|

|

|

I declare, under the penalties of perjury, that this return (including any accompanying schedules and statements) has been examined by me and to the best of my knowledge and belief is a true, correct and complete return.

Date |

Taxpayer’s Signature |

Make check payable to Kentucky State Treasurer.

Mail return with check to: Department of Revenue

Frankfort, Kentucky 40619

NOTICE

This form is to be filed only by persons or firms liable for use tax who are not: (1) registered consumers or (2) registered retailers. Registered consumers and retailers must use returns mailed to them by the Department, or filed electronically.

INSTRUCTIONS

Time and Place for

Tax

Sale

Tangible Personal Property, Digital Property, and Extended Warranty

Completing the

Penalties and

The penalty for failure to pay the tax within the time prescribed is 2 percent of the tax not timely paid for each 30 days payment is

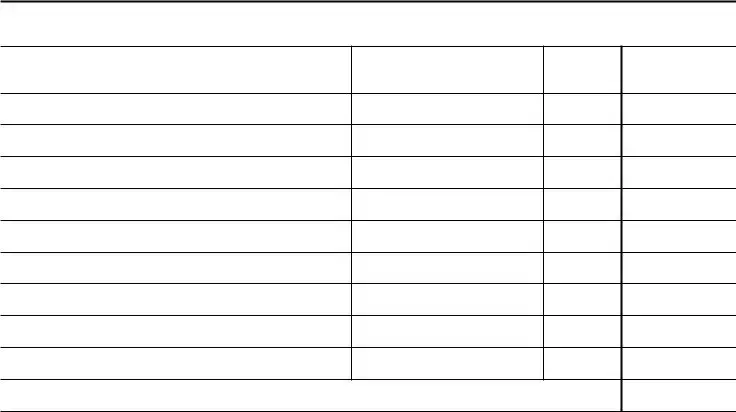

Additional Space for Listing Tangible Personal Property, Digital Property, and

Extended Warranty Services Subject to Use Tax

Name and Address of Seller

Description of Property

Date of

Purchase

Sale Price of

Property and Services

Purchased

$

Subtotal: Sale price of purchases (include in total on Line 1, front page) .............................................

$

| Fact Name | Detail |

|---|---|

| Form Title | Consumer’s Use Tax Return |

| Form Number | 51A113(O) |

| Relevance | This form is used by individuals or firms in Kentucky for use tax purposes who are not registered as consumers or retailers. |

| Use Tax Rate | 6% on the sales price of tangible personal property, digital property, and extended warranty services purchased without sales tax. |

| Applicable Items | Tangible personal property, digital property, and extended warranty services. |

| Due Date | 20 days following the month in which the applicable purchases were made. |

| Governing Law | KRS 139 and KRS 138.460 for tangible personal property and digital property subject to use tax. |

| Penalties and Interest | Late filing penalty is 2% of the tax for each 30 days past due, not exceeding 20% or less than $10. Late payment penalty is similarly calculated. |

| Compensation Limit | Compensation for filing cannot exceed $50. |

| Submission Details | Form and payment should be mailed to the Department of Revenue, Frankfort, Kentucky 40619, payable to the Kentucky State Treasurer. |

After acquiring tangible personal property, digital property, or extended warranty services upon which Kentucky sales or use tax has not been paid, individuals or businesses not registered as consumers or retailers with the Kentucky Department of Revenue must report and pay use tax using form 51A113. This form ensures compliance with state tax laws, and its proper completion helps avoid potential penalties and interest for late or incorrect filing. Here's a straightforward step-by-step guide for filling out the Kentucky 51A113 form.

By carefully following these steps, you can successfully complete and submit your Kentucky 51A113 use tax return. Remember, compliance with tax regulations not only fulfills your legal obligations but also contributes to the common good by ensuring that the necessary funds are available for public services and infrastructure.

FAQs about the Kentucky 51A113 Form

What is the purpose of the Kentucky 51A113 form?

The Kentucky 51A113 form is designed for the specific use of reporting and paying consumer’s use tax to the Commonwealth of Kentucky. Use tax applies to purchases of tangible personal property, digital property, and extended warranty services that are used, stored, or consumed in Kentucky when Kentucky sales tax has not been collected by the seller at the time of purchase. This form is crucial for ensuring that all applicable taxes are duly reported and paid to the Kentucky Department of Revenue.

Who needs to file the Kentucky 51A113 form?

This form must be filed by individuals or businesses that have made purchases subject to use tax and are not registered as consumers or retailers with the Department of Revenue. Essentially, if you or your business has purchased taxable goods or services for use in Kentucky from vendors who did not charge Kentucky sales tax, you are required to report and remit the appropriate use tax using this form.

How is the use tax rate calculated on the form?

The use tax rate is 6 percent of the sales price of all tangible personal property, digital property, and extended warranty services purchased during the month. The sales price is the total cost of the items to the purchaser, after subtracting any cash discounts, valued in money or otherwise. This percentage is applied to the total sale price of items listed on Line 1 of the form to calculate the amount of use tax owed.

Can compensation be deducted on this form?

Yes, compensation can be deducted on the Kentucky 51A113 form. This deduction is calculated as 1 3/4% of the first $1,000 of tax, and 1.5% over $1,000. However, it’s important to note that the total compensation claimed cannot exceed $50. Additionally, this compensation is only allowable if the tax is paid on or before its due date. If the tax payment is late, you are not eligible to claim this compensation.

What are the penalties and interest for late filing or payment?

Penalties for filing the 51A113 form late are calculated at 2 percent of the tax due for each 30 days (or fraction thereof) past the due date, not exceeding 20 percent of the tax. If this calculated penalty is less than $10, a minimum penalty of $10 is applied. Interest is charged on late payments and is calculated based on the annual interest percentage rate divided by 365, multiplied by the number of days late and the tax amount. Additionally, a penalty for late payment is imposed at 2 percent of the unpaid tax for each 30 days the payment is late, with a minimum charge of $10.

Where and when should the Kentucky 51A113 form be filed?

The form should be mailed to the Department of Revenue, Frankfort, Kentucky 40619. It is due 20 days following the month in which the taxable purchase was made. Timely filing and payment are crucial to avoid penalties and interest. A check for the total amount due, payable to the Kentucky State Treasurer, should accompany the form.

When it comes to filling out the Kentucky 51A113 form for consumer's use tax, many individuals find themselves making common mistakes that could have been easily avoided. Here is a look at six of these common mistakes:

Avoiding these common mistakes is essential for correctly completing the Kentucky 51A113 form. Each detail matters, from thoroughly reading the instructions to accurately calculating the tax and ensuring all mandatory fields are filled out. By paying close attention to the instructions provided and double-checking all entered information, filers can properly fulfill their use tax obligations with confidence.

When businesses or individuals fulfill their tax obligations in Kentucky, especially regarding the use tax as stipulated by the Kentucky 51A113 form, a variety of additional documents and forms may come into play. These documents are essential for accurately reporting and paying taxes due on out-of-state purchases or those for which sales tax was not collected at the point of sale. Understanding each document's purpose can streamline the tax filing process, ensuring compliance with Kentucky's Department of Revenue requirements.

Each of these forms plays a specific role in the broader context of tax administration for businesses operating within Kentucky. By familiarizing themselves with the relevant documents, taxpayers can ensure they meet their tax reporting and payment obligations accurately and on time, thereby avoiding potential penalties for non-compliance. It’s advisable to consult with a tax professional or the Department of Revenue if there are any uncertainties regarding which forms are necessary for your specific situation.

The Kentucky 51A113 form is similar to the Sales and Use Tax Return forms used in other states, such as California's BOE-401-A2 form. Both forms are designed for the reporting and payment of taxes on purchases where sales tax was not collected at the time of sale. They require detailed information about the purchases, including the date, price, and description of the property or services bought, as well as the seller's information. The main purpose of these forms is to ensure that tax is collected on all taxable transactions, irrespective of where the purchase was made.

Another similar document is the Consumer Use Tax Return form used in states like Colorado, known as the DR 0252 form. This form, like the Kentucky 51A113, is dedicated to consumers who have purchased goods, digital property, or services for use, storage, or consumption within the state without paying the state's sales tax at the time of purchase. Both forms calculate the tax owed based on the purchase price of the taxable items and require payment to the state's department of revenue.

The New York State ST-120.1 form, or the Use Tax Return for Purchases of Taxable Services from Out-of-State Sellers, also shares similarities with the Kentucky 51A113 form. Both documents are pivotal in situations where residents buy taxable goods or services from outside the state and need to comply with their state's use tax laws. Each form includes sections for documenting the specifics of each purchase that led to use tax liability, thus facilitating compliance with state tax regulations.

Florida’s DR-15MO form, or the Out-of-State Purchase Returns for tax collection, parallels the Kentucky 51A113 form in purpose and structure. They are both designed for reporting and remitting taxes due on out-of-state purchases that were not subject to sales tax at the point of sale. These documents play a crucial role in ensuring fair tax collection from transactions beyond state borders that are used, consumed, or stored within the taxpayer’s state.

The Michigan Use Tax Form 3372, used for reporting purchases subject to the Michigan use tax, closely resembles Kentucky's 51A113 form. Each form is geared towards capturing information on taxable transactions that did not incur sales tax at the point of sale, such as online purchases from out-of-state sellers. They both serve as tools for states to collect taxes on goods and services brought into the state that haven't already been taxed, thus leveling the playing field between in-state and out-of-state purchases.

Similarly, the Illinois Form ST-44, Illinois Use Tax Return, is akin to the Kentucky 51A113 form. Both are intended for individuals and businesses that have made taxable purchases from merchants who did not collect sales tax at the point of sale. The forms require the taxpayer to list these purchases and calculate the use tax owed to the state, ensuring that all applicable transactions are properly taxed in accordance with state laws.

Lastly, the Pennsylvania Use Tax Return (PA-1) shares objectives and functionalities with the Kentucky 51A113 form. It is designed for taxpayers to report and pay tax on purchases made outside of Pennsylvania—for personal or business use—where sales tax was not paid to the seller. Both forms are integral in capturing tax revenue from cross-border and online transactions, ensuring that the use tax complements the sales tax system to tax all eligible purchases equally.

When completing the Kentucky 51A113 form, which is dedicated to the Consumer's Use Tax Return, it is vital to ensure accuracy and compliance with the directives provided by the Commonwealth of Kentucky Department of Revenue. This form is crucial for individuals and firms liable for use tax on purchases of tangible personal property, digital property, and extended warranty services where Kentucky sales or use tax has not been paid. The following list outlines the dos and don'ts to consider:

Following these guidelines will help ensure that your Kentucky 51A113 form is completed accurately and submitted in compliance with state requirements, thereby avoiding any unnecessary complications with your tax obligations.

When it comes to tax forms and their requirements, misconceptions can easily arise, leading to confusion and potential missteps in compliance. The Kentucky 51A113 form, a document designed for reporting use tax on purchases of tangible personal property, digital property, and extended warranty services, is no exception. Here are five common misconceptions about the Kentucky 51A113 form and the truths behind them:

This statement isn't entirely accurate. The Kentucky 51A113 form is used to report purchases subject to use tax, but not all purchases require this. Use tax is due only on purchases for which Kentucky sales tax was not paid at the time of purchase. If the item purchased is exempt from sales tax, it is also exempt from use tax.

While the form is commonly used by businesses, it's a misconception that it's exclusively for them. Individuals who make purchases that are subject to use tax and for which no sales tax was paid at the time of purchase must also file form 51A113. This includes both personal and business-related purchases.

Although tax forms can be intimidating, the 51A113 form is designed to be straightforward. The instructions on the reverse side of the form provide guidance on how to complete it, making it manageable for most individuals and businesses without the need for an accountant. Effort and attentiveness can generally lead to successful self-filing.

A common misunderstanding is that use tax functions as a double tax. In reality, use tax complements sales tax and is only applied to purchases that have not already been taxed through sales tax. Its purpose is to level the playing field for in-state and out-of-state businesses, ensuring that use tax is paid only if sales tax has not been.

Some might underestimate the consequences of not filing the 51A113 form. However, penalties and interest for failing to report and pay use tax can add up significantly over time. The penalty for failure to file by the due date is 2 percent of the tax for each 30 days or fraction thereof, not to exceed 20 percent of the tax, with a minimum penalty of $10. Interest is also charged on late payments, making it financially prudent to file and pay on time.

Understanding these points can help in correctly navigating the responsibilities related to the Kentucky 51A113 form and in ensuring compliance with state tax laws. An informed approach to tax obligations helps prevent unnecessary penalties and fosters a better understanding of the tax system.

Filling out the Kentucky 51A113 form, officially known as the "Consumer’s Use Tax Return," requires careful attention to detail and an understanding of what is expected by the Commonwealth of Kentucky Department of Revenue. Here are several critical takeaways to ensure compliance and accuracy in filing:

Ensuring compliance with Kentucky's use tax laws by accurately completing and timely submitting the 51A113 form is critical for both individuals and businesses. It not only fulfills legal obligations but also supports the provision of vital state services funded by tax revenues. Always consult with a tax professional if you have specific questions or need guidance tailored to your particular situation.

30 Day Notice to Vacate Kentucky - Addresses the final stage of eviction, focusing on the physical retrieval of property as mandated by Kentucky courts.

How to Claim Unclaimed Money in Kentucky - Safeguards the rights of property owners by ensuring their assets are reported and can be claimed in the future.

Kentucky Eviction Laws - It serves as a statutory reminder of the importance of following legal procedures in property eviction cases.