Kentucky 740 Np PDF Template

Kentucky 740 Np PDF Template

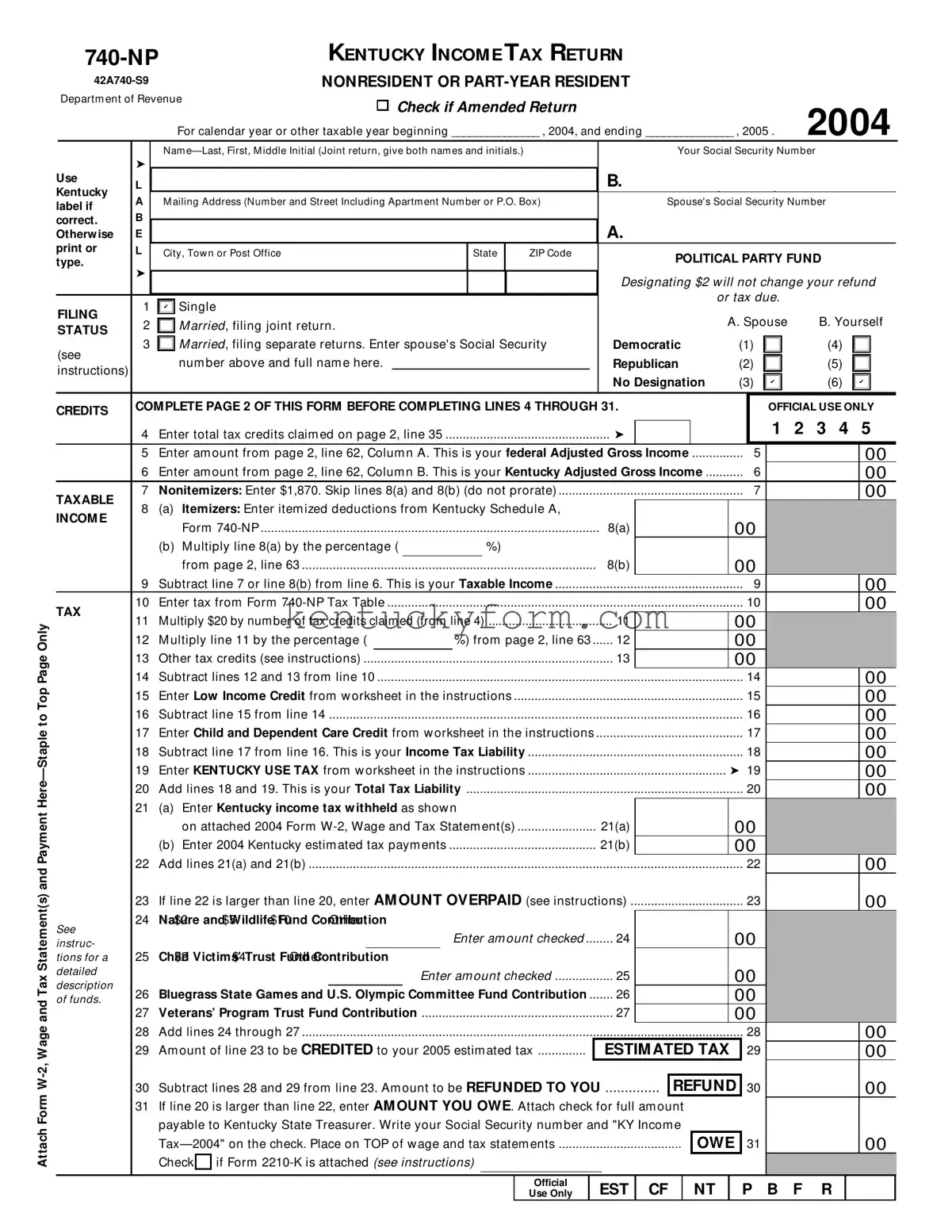

At the heart of taxpayer obligations for those who earn income within the borders of Kentucky but reside there either partially throughout the year or not at all, lies the Kentucky 740 NP form, an essential document for nonresidents and part-year residents to acquaint themselves with. This form stands as a gateway for individuals to accurately report their incomes, claim deductions, and navigate their tax responsibilities in compliance with the Kentucky Department of Revenue. Embodied within this document are various sections designed for meticulous reporting: attachments of W-2s, precise income calculations, claims for tax credits, and distinctive options for designating contributions to state funds, all underscore the form's comprehensive nature. Notably, the form caters to various filing statuses and uniquely accommodates contributions to political party funds without affecting the filer's tax liability or refund. Additionally, with provisions for amending returns, it underscores the state's recognition of the dynamism in taxpayers' lives. Moreover, the intersection of multiple state tax considerations, evident in reciprocal state resident reporting, illustrates the layered complexity of state income taxation. Inherently, the 740-NP form embodies a blend of compliance, choice, and correction, framing the fiscal interaction between the commonwealth and its nonresident earners in a structured yet flexible manner.

Attach Form

|

|

KENTUCKY INCOM E TAX RETURN |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

NONRESIDENT OR |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

Departm ent of Revenue |

|

|

|

|

¸ Check if Amended Return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2004 |

|||||||||||||||||

|

|

|

|

For calendar year or other taxable year beginning _______________ , 2004, and ending _______________ , 2005 . |

|

||||||||||||||||||||||||||||||||||

|

|

|

Nam |

|

|

|

|

|

|

|

Your Social Security Num ber |

|

|

|

|

|

|||||||||||||||||||||||

Use |

➤ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

L |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Kentucky |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

A |

|

M ailing Address (Num ber and Street Including Apartm ent Num ber or P.O. Box) |

|

|

|

Spouse's Social Security Num ber |

|

|

|

|

|

||||||||||||||||||||||||||||

label if |

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

correct. |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Otherw ise |

E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

print or |

L |

|

City, Tow n or Post Office |

|

|

|

State |

|

ZIP Code |

|

|

|

|

POLITICAL PARTY FUND |

|

|

|

|

|

||||||||||||||||||||

type. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

➤ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Designating $2 w ill not change your refund |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or tax due. |

|

|

|

|

|

|

|

||||||

|

1 |

|

|

Single |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

✔ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

FILING |

2 |

|

|

M arried, filing joint return. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. Spouse |

|

B. Yourself |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

STATUS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

3 |

|

|

M arried, filing separate returns. Enter spouse's Social Security |

Democratic |

(1) |

|

|

|

|

|

(4) |

|

|

|

|

||||||||||||||||||||||||

(see |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

num ber above and full nam e here. |

|

|

|

|

|

|

|

|

|

Republican |

(2) |

|

|

|

|

|

(5) |

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

No Designation |

(3) |

|

|

|

|

|

(6) |

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

✔ |

|

|

|

|

✔ |

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

CREDITS |

COM PLETE PAGE 2 OF THIS FORM BEFORE COM PLETING LINES 4 THROUGH 31. |

|

|

|

|

OFFICIAL USE ONLY |

|||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

Enter total tax credits claim ed on page 2, line 35 |

|

|

➤ |

|

|

|

|

|

|

|

|

|

1 |

|

2 |

3 |

4 |

|

5 |

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

5 |

|

Enter am ount from page 2, line 62, Colum n A. This is your federal Adjusted Gross Income |

5 |

|

|

|

|

|

|

|

00 |

|||||||||||||||||||||||||||

|

6 |

|

Enter am ount from page 2, line 62, Colum n B. This is your Kentucky Adjusted Gross Income |

6 |

|

|

|

|

|

|

|

00 |

|||||||||||||||||||||||||||

TAXABLE |

7 |

|

Nonitemizers: Enter $1,870. Skip lines 8(a) and 8(b) (do not prorate) |

|

|

|

|

|

7 |

|

|

|

|

|

|

|

00 |

||||||||||||||||||||||

INCOM E |

8 |

|

(a) |

Itemizers: Enter item ized deductions from Kentucky Schedule A, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

Form |

|

|

|

|

|

|

|

|

|

8(a) |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

(b) |

M ultiply line 8(a) by the percentage ( |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

from page 2, line 63 |

|

|

|

|

|

|

|

|

8(b) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

9 |

|

Subtract line 7 or line 8(b) from line 6. This is your Taxable Income |

|

|

|

|

|

9 |

|

|

|

|

|

|

|

00 |

||||||||||||||||||||||

TAX |

10 |

|

Enter tax from Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10 |

|

|

|

|

|

|

|

00 |

|||||||||||||

11 |

|

M ultiply $20 by num ber of tax credits claim ed (from line 4) |

|

|

11 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

12 |

|

M ultiply line 11 by the percentage ( |

|

|

|

%) from page 2, line 63 |

12 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

13 |

|

Other tax credits (see instructions) |

|

|

|

|

|

|

|

|

13 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

14 |

|

Subtract lines 12 and 13 from line 10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 |

|

|

|

|

|

|

|

00 |

|||||||||||||

|

15 |

|

Enter Low Income Credit from w orksheet in the instructions |

|

|

|

|

|

|

|

|

15 |

|

|

|

|

|

|

|

00 |

|||||||||||||||||||

|

16 |

|

Subtract line 15 from line 14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 |

|

|

|

|

|

|

|

00 |

|||||||||||||

|

17 |

|

Enter Child and Dependent Care Credit from w orksheet in the instructions |

|

|

|

|

|

17 |

|

|

|

|

|

|

|

00 |

||||||||||||||||||||||

|

18 |

|

Subtract line 17 from line 16. This is your Income Tax Liability |

|

|

|

|

|

|

|

|

18 |

|

|

|

|

|

|

|

00 |

|||||||||||||||||||

|

19 |

|

Enter KENTUCKY USE TAX from w orksheet in the instructions |

|

|

|

|

|

|

|

|

➤ 19 |

|

|

|

|

|

|

00 |

||||||||||||||||||||

|

20 |

|

Add lines 18 and 19. This is your Total Tax Liability |

|

|

|

|

|

|

|

|

20 |

|

|

|

|

|

|

|

00 |

|||||||||||||||||||

|

21 |

|

(a) |

Enter Kentucky income tax w ithheld as show n |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

on attached 2004 Form |

|

|

21(a) |

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

(b) |

Enter 2004 Kentucky estim ated tax paym ents |

|

|

21(b) |

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

22 |

|

Add lines 21(a) and 21(b) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22 |

|

|

|

|

|

|

|

00 |

|||||||||||||

|

23 |

|

.................................If line 22 is larger than line 20, enter AM OUNT OVERPAID (see instructions) |

23 |

|

|

|

|

|

|

|

00 |

|||||||||||||||||||||||||||

See |

24 Nature and Wildlife Fund Contribution |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

¸ $2 |

¸ $5 |

¸ $10 ¸ Other |

|

|

|

Enter am ount checked |

24 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

instruc- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

tions for a |

25 |

|

Child Victims’ Trust Fund Contribution |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

detailed |

|

¸ $2 |

¸ $4 |

¸ Other |

|

|

Enter am ount checked |

25 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

description |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

26 |

|

Bluegrass State Games and U.S. Olympic Committee Fund Contribution |

26 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

of funds. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

27 |

|

Veterans’ Program Trust Fund Contribution |

........................................................ |

|

|

|

|

|

|

|

27 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

28 |

|

Add lines 24 through 27 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

28 |

|

|

|

|

|

|

|

00 |

||||||||||||

|

29 |

|

..............Am ount of line 23 to be CREDITED to your 2005 estim ated tax |

|

ESTIM ATED TAX |

|

29 |

|

|

|

|

|

|

|

00 |

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30 |

|

Subtract lines 28 and 29 from line 23. Am ount to be REFUNDED TO YOU |

.............. |

|

|

REFUND |

30 |

|

|

|

|

|

|

|

00 |

|||||||||||||||||||||||

31If line 20 is larger than line 22, enter AM OUNT YOU OWE. Attach check for full am ount payable to Kentucky State Treasurer. Write your Social Security num ber and "KY Incom e

OWE 31 |

00 |

|

Check ¸ if Form |

|

|

Official |

|

|

Use Only |

EST CF NT P B F |

R |

FORM

<www.revenue.ky.gov

Page 2

A copy of pages 1 and 2 of your federal income tax return and all supporting schedules must be attached to Kentucky Form

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RESIDENCY |

¸ |

|

|

|

|

|

. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

✔ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

STATUS |

¸ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||

(check |

|

|

M oved into Kentucky |

/ |

|

|

/ |

|

|

04 |

|

. State m oved from |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

M oved out of Kentucky |

/ |

|

|

/ |

|

|

04 |

|

. State m oved to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

one box) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

¸ |

➤ |

|

IL |

|

|

IN |

|

|

|

M I |

|

|

OH |

|

|

VA |

|

WV |

|

|

|

WI |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

filed w ith your state of residence and circle the state of residence. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||

CREDITS |

32 |

|

(a) |

Credits for yourself: |

|

¸ |

Regular |

|

|

¸ |

|

¸ |

Check both if 65 or over |

|

|

¸ |

|

¸ |

Check both if blind |

|

|

|

Enter num ber of |

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Check both if blind |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Regular |

|

|

¸ |

|

¸ |

Check both if 65 or over |

|

|

¸ |

|

¸ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

(b) |

Credits for spouse: |

|

¸ |

|

|

|

|

|

|

|

boxes checked |

32 |

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

33 |

|

Nam es of dependent children: (a) |

|

|

|

|

|

|

|

|

|

|

|

(b) |

|

(c) |

|

|

|

|

|

|

|

|

|

|

|

(d) |

|

|

|

|

|

|

|

|

|

|

|

|

Total |

33 |

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

|

34 |

|

Tax credits for other dependents |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

34 |

|

|

|

|

|

||||||||||||||||||||||||

|

35 |

|

Add the total num ber of tax credits claim ed on lines 32, 33 and 34 above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35 |

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

INCOM E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. Total from Attached |

|

|

|

|

|

B. Kentucky |

|

|

|

||||||||||||||||||||||||||

|

36 |

|

Enter all w ages, salaries, tips, etc. (attach w age and tax statem ents) |

|

|

|

|

|

|

|

|

|

|

|

Federal Return |

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

Do not include m oving expense reim bursem ents |

|

|

|

|

|

36 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

37 |

|

M oving expense reim bursem ent (attach Schedule M E) |

|

|

|

|

|

37 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

38 |

|

Interest and dividends |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||

|

39 |

|

Business incom e or (loss) (attach Schedule C or |

|

|

|

|

|

39 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

40 |

|

Capital gain or (loss) (attach Schedule D) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||

|

41 |

|

Other gains or (losses) (attach Form 4797) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

41 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||

|

42 |

|

(a) |

Federally taxable IRA distributions, pensions and annuities |

|

|

|

|

|

42(a) |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

(b) |

Pension incom e exclusion (attach Schedule P if m ore than $40,200) ... |

42(b) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 ) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||

|

43 |

|

Rents, royalties, partnerships, estates, trusts, etc. (attach federal Schedule E) ... |

43 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

44 |

|

Farm incom e or (loss) (attach Schedule F) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

44 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||

|

45 |

|

Other incom e (list type and am ount) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

45 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||

|

46 |

|

Com bine lines 36 through 45. This is your Total Income |

|

|

|

|

|

46 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

ADJUST- |

47 |

|

Educator expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

47 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

M ENTS |

48 |

|

Certain business expenses of reservists, perform ing artists and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

TO |

|

|

|

|

|

|

|

|

48 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

INCOM E |

49 |

|

IRA deduction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

49 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

50 |

|

Student loan interest deduction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

50 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||||||||||

|

51 |

|

Tuition and fees deduction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

51 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||||||||||

|

52 |

|

Health savings account deduction (attach federal Form 8889) |

|

|

|

|

|

52 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

53 |

|

M oving expenses (attach Schedule M E) |

................................................................ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

53 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||||||||||||

|

54 |

|

Deduction for |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

54 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||

|

55 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

55 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||

|

56 |

|

|

|

|

|

|

56 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||

|

57 |

|

Penalty on early w ithdraw al of savings |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

57 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||

|

58 |

|

Alim ony paid (recipient's nam e and Social Security num ber) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

58 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||

|

59 |

|

|

|

|

|

|

59 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

60 |

|

Health insurance prem ium s (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||

|

61 |

|

Add lines 47 through 60. Total adjustm ents to incom e |

|

|

|

|

|

61 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

62 |

|

Subtract line 61 from line 46. This is your Adjusted Gross Income |

|

|

|

|

|

62 |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

63 |

|

Divide line 62, Colum n B, by line 62, Colum n A. If am ount is equal to or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

greater than 100%, enter 100%. This is your Percentage of Kentucky |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

63 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

% |

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

Adjusted Gross Income to Federal Adjusted Gross Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I, the undersigned, declare under penalties of perjury that I have exam ined this return, including all accom panying schedules and statem ents, and to the best of m y know ledge and belief, it is true, correct and com plete. I also understand and agree that our election to file a joint return under the provisions of Regulation 103 KAR 17:020 w ill result in refunds being m ade payable to us jointly and in each of us being jointly and severally liable for all taxes accruing under this return.

➤ |

➤ |

* |

|

Your Signature (If joint return, both m ust sign.) |

Spouse's Signature |

Telephone Number (daytime) |

Date Signed |

|

|

|

|

Typed or Printed Nam e of Preparer Other than Taxpayer |

I.D. Num ber of Preparer |

|

Date |

➤ M ail refund returns to Kentucky Department of Revenue, Frankfort, KY |

➤ M ake check payable to |

M ail returns w ith payment to Kentucky Department of Revenue, Frankfort, KY |

Kentucky State Treasurer. |

| Fact Name | Detail |

|---|---|

| Form Purpose | The 740-NP form is for nonresidents or part-year residents who need to file Kentucky income tax returns. |

| Amended Returns | There is an option to check if the submission is an amended return, indicating corrections to a previously filed 740-NP form. |

| Filing Status Options | Includes single, married filing jointly, and married filing separately, with designated spaces for spouse's information if applicable. |

| Political Party Fund | Taxpayers can designate $2 to a political party fund without affecting their refund or tax due. |

| Income Calculation | Requires both federal Adjusted Gross Income and Kentucky Adjusted Gross Income for accurate state tax calculations. |

| Tax Credits and Deductions | Offers specific lines for claiming tax credits, including instructions for calculating the Low Income Credit and Child and Dependent Care Credit. |

| Contributions to State Funds | Allows contributions to various Kentucky-specific funds such as the Nature and Wildlife Fund, Child Victims' Trust Fund, and Veterans' Program Trust Fund. |

| Attachment Requirements | A copy of pages 1 and 2 of the federal income tax return and all supporting schedules must be attached to the 740-NP form. |

Filing the Kentucky 740-NP form is necessary for nonresidents or part-year residents who have earned income in Kentucky during the tax year. This process can seem complex, but breaking it down into manageable steps can simplify the task. Carefully completing this form is crucial to ensure accurate tax liability calculation and avoid potential issues with the Department of Revenue. Below are step-by-step instructions to help you fill out the Kentucky 740-NP form correctly.

By following these detailed steps, you can accurately complete and submit your Kentucky 740-NP form. This task can be managed more efficiently by gathering all necessary documentation before beginning and carefully reviewing the form's instructions. Remember, accuracy is crucial in tax filing to ensure compliance with the law and secure any refunds due.

FAQ Section: Kentucky 740 NP Form

The Kentucky 740 NP Form is an income tax return document specifically designed for nonresidents or part-year residents of Kentucky. It allows these individuals to accurately report their income earned in Kentucky during the tax year. The form is used to calculate the Kentucky income tax owed based on the portion of income attributable to Kentucky sources.

This form is intended for individuals who are either not full-year residents of Kentucky or who have resided in the state for only part of the tax year. Full-year nonresidents who have earned income from Kentucky sources and part-year residents who have earned income both within and outside of Kentucky during the tax year must complete and file this form. It's important to attach any required documents, such as W-2s or other tax statements, to accurately report income.

To calculate your Kentucky tax credits on the Form 740 NP, you will need to complete page 2 of the form first. The total tax credits claimed will be reported on line 4 of the form. These credits could include allowances for personal exemptions, dependents, and potentially other state-specific credits. It is essential to follow the instructions and worksheets provided in the form's guidelines to accurately determine your eligible tax credits.

If you realize that you've made a mistake on your already filed Kentucky 740 NP Form, you should file an amended return. To do this, check the box indicating an amended return at the top of a new 740 NP Form and correct the information. You should include any additional documentation that supports the changes made. The amended return will allow the Kentucky Department of Revenue to correct your tax record based on the updated information provided.

One common mistake individuals encounter when completing the Kentucky 740-NP form, particularly nonresidents or part-year residents, is misunderstanding their filing status. Properly identifying whether you are a full-year nonresident, part-year resident, or a full-year resident of a reciprocal state is crucial because it determines the tax obligations and potential benefits you may qualify for. An incorrect filing status can lead to errors in tax liability calculations, potentially resulting in either underpayment or overpayment of taxes.

Another area that frequently causes confusion is the handling of income and deductions. Taxpayers must carefully report all wages, salaries, tips, and other forms of income, ensuring that these amounts are accurately transferred from federal returns. Deductions, on the other hand, often get mishandled, particularly when itemizing or deciding between Kentucky-specific deductions and standard deduction amounts. Failing to correctly adjust your income can significantly impact your taxable income and the amount of tax owed.

Additionally, many individuals forget to attach necessary documentation, such as Form W-2, Wage and Tax Statement(s), and copies of pages 1 and 2 of their federal return, alongside all supporting schedules. This oversight can lead to processing delays or requests for additional information, complicating what could otherwise be a straightforward filing process. It's a simple step but crucial for a smooth submission.

Lastly, misunderstandings or overlooks regarding tax credits and payments can be detrimental. It's vital to correctly calculate and claim any eligible tax credits, such as the child and dependent care credit or credits for other dependents. Furthermore, accurately reporting Kentucky income tax withheld and estimated tax payments is essential. These figures not only affect your total tax liability but also influence any potential refund or amount owed, making precision paramount.

When filing the Kentucky 740 NP form, a nonresident or part-year resident income tax return, it's important to be aware of other relevant documents that may need to be prepared and submitted alongside it. These documents support, validate, or otherwise complement the information provided in the 740 NP form. Knowing what these documents are and their purpose can streamline the tax preparation process and ensure compliance with Kentucky's tax regulations. Below is a list of documents often used in conjunction with the Kentucky 740 NP form.

Together, these documents provide a comprehensive framework for accurately reporting income, deductions, and credits related to Kentucky state taxes for nonresidents or part-year residents. Ensuring that all relevant forms and schedules are correctly filled out and attached where necessary is crucial for the accurate processing of your Kentucky state tax return.

The IRS Form 1040NR, U.S. Nonresident Alien Income Tax Return, shares similarities with the Kentucky 740-NP form as they both are dedicated to individuals who do not reside within the jurisdiction but have earned income from it. These forms calculate the tax liability based on the income earned within the respective territories (United States for the 1040NR and Kentucky for the 740-NP) and include provisions for various deductions and credits to determine the final tax liability.

California Form 540NR, Nonresident or Part-Year Resident Income Tax Return, is also similar to the Kentucky 740-NP form. Like the Kentucky form, this document is used by individuals who either lived in California for only part of the year or earned income in the state without being residents. Both forms adjust taxable income based on the portion attributable to the state, allowing nonresidents and part-year residents to file taxes specific to the income earned within the state.

The IRS Schedule C (Profit or Loss from Business) is used to report income or loss from a business operated or a profession practiced as a sole proprietor. While the Kentucky 740-NP form itself is not specifically for businesses, it requires information from federal schedules, including income or loss reported on Schedule C, to accurately report and tax income derived from Kentucky sources.

The IRS Form 2106 (Employee Business Expenses) is required for individuals to itemize work-related expenses that are not reimbursed by their employer. The relevance to the Kentucky 740-NP form comes into play as certain adjustments to income on the federal level, including those documented on Form 2106, impact the Adjusted Gross Income (AGI) reported on state tax forms including the 740-NP, affecting the taxable income calculation for the state.

Form W-2, Wage and Tax Statement, directly ties to both federal and state tax forms like the Kentucky 740-NP. This document details an employee's income and withheld taxes for the year. For the 740-NP, the Form W-2 provides essential information regarding income earned and taxes already paid, crucial for calculating the taxpayer's liability or refund due from Kentucky.

The IRS Schedule SE (Self-Employment Tax) is another document with a connection to the Kentucky 740-NP form. Self-employed individuals use Schedule SE to calculate the tax due on net earnings from self-employment. While Kentucky's form does not directly calculate self-employment tax, the income and deductions reported on Schedule SE affect the AGI, which is a critical component of the Kentucky 740-NP.

IRS Form 2210 (Underpayment of Estimated Tax by Individuals, Estates, and TrusteS) relates to Kentucky 740-NP through the calculation and reporting of estimated tax payments. Taxpayers who do not have sufficient income tax withheld throughout the year may need to make estimated tax payments to avoid underpayment penalties. The 740-NP addresses this scenario through its section for reporting estimated payments made to Kentucky.

The IRS Form 1099 series, which documents various types of income other than wages, salaries, and tips, impacts the reporting on Kentucky 740-NP similarly. Information from 1099 forms, such as dividends, interest, and miscellaneous income, must be reported on the 740-NP if this income is attributable to sources within Kentucky, affecting the state income tax calculation.

IRS Form 4868 (Application for Automatic Extension of Time To File U.S. Individual Income Tax Return) shares a procedural relation with the Kentucky 740-NP form. If a taxpayer files Form 4868 for a federal extension, they typically need to do so for the state return as well. The 740-NP instructions include guidelines for taxpayers who have obtained a federal extension, indicating how to handle filing deadlines for the Kentucky return.

Finally, the IRS Schedule A (Itemized Deductions) is closely related to parts of the Kentucky 740-NP form. Taxpayers who itemize deductions on the federal level with Schedule A can often deduct some of those expenses on their state return as well. The 740-NP form considers these federal itemizations in adjusting state taxable income, especially with deductions that are also recognized by Kentucky tax law.

Filling out the Kentucky 740 NP form, a document necessary for nonresidents or part-year residents reporting income tax in Kentucky, requires careful attention to detail. Below are pivotal do's and don'ts that can guide you through the process, ensuring accuracy and compliance.

Remember, the Kentucky 740 NP form is a critical document that requires your full attention and accuracy. By following the guidelines above, you can navigate the complexities of tax filing with confidence, ensuring compliance and potentially maximizing your benefits under the law.

When it comes to completing tax forms like the Kentucky 740-NP, misinformation can easily spread, leading to common misunderstandings. It's essential to debunk these myths to ensure individuals file their taxes correctly and efficiently. Here are four misconceptions about the Kentucky 740-NP Form, explained for better clarity:

Understanding these nuances about the Kentucky 740-NP form can help taxpayers avoid common pitfalls and file their taxes more accurately. Whether you're a full-year resident, a nonresident, or a part-year resident, it's important to review the form and its instructions thoroughly to ensure compliance with Kentucky's tax laws.

Filling out and using the Kentucky 740 NP form is a process that requires careful attention to detail. Whether you're a nonresident or part-year resident of Kentucky, this form is crucial for reporting your income tax to the state. Here are a few key takeaways to keep in mind:

Understanding these key points can simplify the process of completing the Kentucky 740 NP form and ensure that nonresidents and part-year residents comply with state tax laws. Always double-check your entries and calculations to avoid errors that could delay processing or result in penalties.

Ky Dog License Shelby County - A well-crafted application enabling Shelby County pet owners to comply with local regulations, ensuring pets are vaccinated and licensed.

Kentucky Driver License - By selecting a driving category, CDL holders in Kentucky actively participate in a system designed to enhance road safety and driver health monitoring.