Kentucky 74A118 PDF Template

Kentucky 74A118 PDF Template

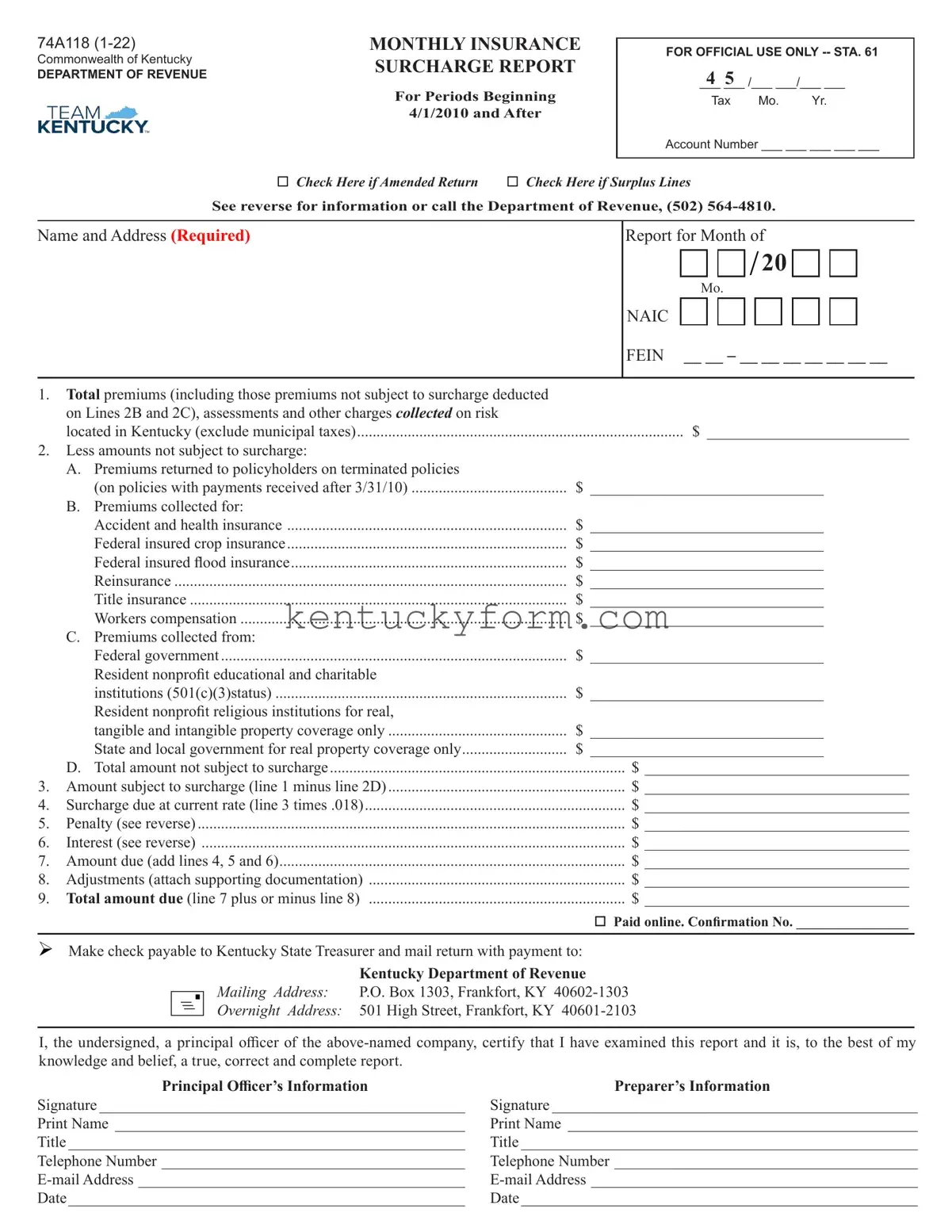

Understanding the Kentucky 74A118 form is pivotal for insurance companies operating within the state. This specific document, officially titled the Monthly Insurance Surcharge Report, is designed for periods starting from April 1, 2010, and forwards, marking a significant component in maintaining compliance with the Commonwealth of Kentucky's Department of Revenue requirements. It serves to detail the total premiums, assessments, and other charges collected on risks located within Kentucky, excluding certain exemptions like municipal taxes, and delineates the process for calculating and reporting the insurance premium surcharge as mandated by the state. Notably, this form outlines the necessary steps for adjustments, indicating whether an amended return is needed or if the report involves surplus lines, all while highlighting vital deductions that can be made from the totals, including premiums returned on terminated policies and charges collected under specific insurance types that are exempt from surcharge. Furthermore, it includes sections for penalties and interest for late submissions or payments, underscoring the importance of timely and accurate filing. As such, insurance providers must familiarize themselves with the form's detailed requirements to ensure they comply with Kentucky law, including the surcharge rates, exemptions, and penalties, thus avoiding potential financial and legal repercussions.

74A118 |

MONTHLY INSURANCE |

Commonwealth of Kentucky |

SURCHARGE REPORT |

DEPARTMENT OF REVENUE |

|

|

For Periods Beginning |

|

4/1/2010 and After |

FOR OFFICIAL USE ONLY

___4 ___5 /___ ___/___ ___

Tax Mo. Yr.

Account Number ___ ___ ___ ___ ___

Check Here if Amended Return |

Check Here if Surplus Lines |

See reverse for information or call the Department of Revenue, (502)

Name and Address (Required)

Report for Month of

/ 20

Mo.

NAIC

FEIN __ __ – __ __ __ __ __ __ __

1.Total premiums (including those premiums not subject to surcharge deducted on Lines 2B and 2C), assessments and other charges collected on risk

located in Kentucky (exclude municipal taxes) |

$ __________________________ |

2.Less amounts not subject to surcharge:

A. Premiums returned to policyholders on terminated policies

|

(on policies with payments received after 3/31/10) |

$ |

______________________________ |

B. |

Premiums collected for: |

|

|

|

Accident and health insurance |

$ |

______________________________ |

|

Federal insured crop insurance |

$ |

______________________________ |

|

Federal insured flood insurance |

$ |

______________________________ |

|

Reinsurance |

$ |

______________________________ |

|

Title insurance |

$ |

______________________________ |

|

Workers compensation |

$ |

______________________________ |

C. |

Premiums collected from: |

|

|

|

Federal government |

$ |

______________________________ |

|

Resident nonprofit educational and charitable |

|

|

|

institutions (501(c)(3)status) |

$ |

______________________________ |

|

Resident nonprofit religious institutions for real, |

|

|

|

tangible and intangible property coverage only |

$ |

______________________________ |

|

State and local government for real property coverage only |

$ |

______________________________ |

|

D. Total amount not subject to surcharge |

$ __________________________________ |

3. |

Amount subject to surcharge (line 1 minus line 2D) |

$ __________________________________ |

4. |

Surcharge due at current rate (line 3 times .018) |

$ __________________________________ |

5. |

Penalty (see reverse) |

$ __________________________________ |

6. |

Interest (see reverse) |

$ __________________________________ |

7. |

Amount due (add lines 4, 5 and 6) |

$ __________________________________ |

8. |

Adjustments (attach supporting documentation) |

$ __________________________________ |

9. |

Total amount due (line 7 plus or minus line 8) |

$ __________________________________ |

Paid online. Confirmation No. ________________

Make check payable to Kentucky State Treasurer and mail return with payment to:

Kentucky Department of Revenue

Mailing Address: P.O. Box 1303, Frankfort, KY

Overnight Address: 501 High Street, Frankfort, KY

I, the undersigned, a principal officer of the

Principal Officer’s Information |

Preparer’s Information |

Signature _______________________________________________ |

Signature _______________________________________________ |

Print Name _____________________________________________ |

Print Name _____________________________________________ |

Title ___________________________________________________ |

Title ___________________________________________________ |

Telephone Number _______________________________________ |

Telephone Number _______________________________________ |

Date___________________________________________________ |

Date___________________________________________________ |

GENERAL INFORMATION

KRS 136.392 requires that every domestic, foreign and alien insurer, other than life and health insurers, which is subject to or exempted from Kentucky insurance premiums taxes as levied pursuant to the provisions of either KRS 136.350, 136.370 or 136.390, shall charge and collect a surcharge at the current rate upon each $100 of premium, assessments or other charges, except for whether the charges are designated as premiums, assessments or otherwise.

Every insurer is required to file for each period, whether filing monthly or annually, even if no premiums were collected.

The insurance premium surcharge shall be collected by the insurer from its policyholders at the same time and in the same manner that its premium or other charge for the insurance coverage is collected. When claiming a deduction for premiums returned to a policyholder, the surcharge must also be returned to the policyholder.

No insurer or its agent shall be entitled to any portion of any premium surcharge as a fee or commission for its collection.

On or before the 20th day of each month, each insurer shall report and remit to the Department of Revenue, on the required forms, all premium surcharge monies collected during the preceding monthly accounting period less any monies returned to policyholders on policies terminated by either the insured or the insurer. Insurers with an annual liability of less than $1,000 for each of the previous two calendar years may report and remit to the Department of Revenue all premium surcharge monies collected on a calendar year basis on or before the 20th day of January of the following year.

Account Number For Surplus Lines

•

•Single

The penalty for failure to file an insurance premium surcharge report by the due date is 2 percent of the surcharge due for each 30 days or fraction thereof that the report is late (maximum 20 percent). The minimum penalty is $10. (KRS 131.180 (1))

The penalty for failure to pay the insurance premium surcharge by the due date is 2 percent of the surcharge due for each 30 days or fraction thereof that the payment is overdue (maximum 20 percent). The minimum penalty is $10. (KRS 131.180 (2))

Interest at the “tax increase rate” is applied to all insurance premium surcharge liabilities not paid by the original due date of the report. The computation period is from the original due date of the report to the date of payment. (KRS 131.183 (1))

Report on line 1 only those premiums that have been collected.

NOTE: Refunds or credits can only be taken on premiums returned to policy holders on terminated policies, not on exempt premiums such as worker’s compensation insurance. Refund requests must be made in writing.

Types of Policyholders Exempt or Partially Exempt from the Insurance Premium Surcharge pursuant to KRS 136.392(5):

•The federal government;

•Resident educational and charitable institutions qualifying under Section 501(c)(3) of the Internal Revenue Code;

•Resident nonprofit religious institutions for real, tangible, and intangible property coverage only;

•State government for coverage of real property; or

•Local governments for coverage of real property.

Also, Exempt from the Insurance Premium Surcharge:

•Premiums received by life and health insurers pursuant to KRS 136.392(1);

•Municipal premium taxes pursuant to KRS 136.392(1);

•Premiums received for accident and health insurance;

•Premiums received for federal insured crop insurance;

•Premiums received for federal insured flood insurance;

•Premiums received for reinsurance;

•Premiums received for title insurance; or

•Premiums received for workers’ compensation insurance.

Premiums collected for surety and bonds on public works projects are subject to the surcharge if the contractor is the policyholder. The fact that a governmental entity may be the obligee has no bearing on the application of the surcharge.

| Fact Name | Detail |

|---|---|

| Form Designation and Purpose | The Kentucky 74A118 form is identified as the Monthly Insurance Surcharge Report, used by insurers to report and remit surcharges collected on insurance premiums, assessments, and other charges for risks located in Kentucky. |

| Governing Law | This form operates under the governance of KRS 136.392, which outlines the requirements for domestic, foreign, and alien insurers, excluding life and health insurers, to charge, collect, report, and remit a surcharge on each $100 of premium or other charges. |

| Exemptions and Deductions | The form allows for certain deductions from the total premiums collected, such as premiums returned on terminated policies and premiums collected for specific types of insurance (e.g., accident and health, federal insured crop and flood insurances, reinsurance, title insurance, and workers’ compensation) and from certain policyholders like the federal government, nonprofit organizations, and state or local governments under specified conditions. |

| Penalties and Interests | Insurers face penalties for failing to file or pay the insurance premium surcharge by the due dates, with specific rates for penalties and interest charges outlined under KRS 131.180 (1) & (2) and KRS 131.183 (1) for overdue surcharges. |

| Submission Procedures | Insurers must report and remit all collected surcharge monies to the Kentucky Department of Revenue monthly or, under certain conditions, on an annual basis if their annual liability is less than $1,000 for each of the previous two calendar years. The form also requires the signature of a principal officer of the insurer, certifying the accuracy of the report. |

The Kentucky 74A118 form is a necessary document for insurance entities within Kentucky to report and remit the monthly insurance surcharge. This step-by-step guide seeks to assist insurance companies in accurately completing this form. Completing the Kentucky 74A118 accurately ensures compliance with the Commonwealth's Department of Revenue requirements and aids in the timely and correct submission of insurance surcharges collected.

Once the Kentucky 74A118 form has been filled out correctly and all necessary documents have been attached, it is essential to mail the form to the Department of Revenue's specified address to complete the submission process. Timely and accurate reporting helps ensure compliance with Kentucky's Department of Revenue regulations and contributes to the smooth operation of the insurance entity's financial responsibilities.

What is the Kentucky 74A118 form?

The Kentucky 74A118 form is a Monthly Insurance Surcharge Report mandated by the Commonwealth of Kentucky's Department of Revenue for domestic, foreign, and alien insurers, excluding those providing life and health insurance. This report, required for each period post-April 1, 2010, involves documenting and remitting surcharges collected from policyholders on various insurance premiums, assessments, and charges, with certain exemptions outlined by the state.

Who needs to file the Kentucky 74A118 form?

All insurance providers operating within Kentucky, apart from those exclusively offering life and health insurance, must file the 74A118 form. This requirement applies regardless of whether premiums have been collected during the reporting period. Insurers must ensure the surcharge is collected alongside premiums or other charges and fully remitted to the Department of Revenue accordingly.

What types of premiums are subject to the Kentucky insurance premium surcharge?

Premiums that are subject to the surcharge include most charges collected on risks located in Kentucky, with notable exclusions. These exclusions comprise premiums returned on terminated policies, accident and health insurance, federal insured crop and flood insurance, reinsurance, title insurance, workers' compensation, and premiums collected from certain government and nonprofit entities. Hence, much of the traditional insurance premium landscape falls under this surcharge's purview.

How is the amount subject to surcharge calculated?

To calculate the amount subject to surcharge, insurers aggregate all premiums, assessments, and other charges collected. From this total, deductions are made for specific non-surchargeable items and exemptions such as returned premiums, accident and health insurance, and others mentioned previously. The resulting figure represents the surchargeable amount, which is then multiplied by the current surcharge rate to determine the surcharge due.

What penalties are associated with late filing or payment?

These penalties underscore the importance of timely reporting and payment to avoid additional financial liabilities.

Are any policyholders exempt from the insurance premium surcharge?

Yes, certain policyholders are wholly or partially exempt from the surcharge. Exemptions are granted to the federal government, resident educational and charitable institutions with Section 501(c)(3) status, resident nonprofit religious institutions for specific property coverage, state government for real property coverage, and local governments for the same. Additionally, specific insurance types, such as life and health insurance, receive automatic exemption from the surcharge.

How should adjustments be reported on the Kentucky 74A118 form?

Adjustments to the surcharge report require supporting documentation and are entered on the form to reflect either an increase or decrease in the total amount due. These adjustments often relate to previously reported figures that have since changed due to various factors like returned premiums or corrections of previously reported amounts. Proper documentation ensures the accuracy and integrity of the surcharge reporting process.

When completing the Kentucky 74A118 form, there are common mistakes that individuals often make, leading to inaccuracies and potential penalties. Understanding these errors can help ensure the form is filled out correctly and submitted on time.

One major mistake is not reporting accurate premium amounts on line 1. This figure should include all premiums, assessments, and other charges collected on risks located in Kentucky, excluding municipal taxes. However, individuals sometimes report incorrect totals either by oversight or misunderstanding of what needs to be included.

Another error involves incorrect deductions on lines 2A through 2C. These lines are designed for deducting amounts not subject to surcharge, such as premiums returned on terminated policies or collected for exempt categories like accident and health insurance. Mistakenly including ineligible deductions or miscalculating these amounts can lead to an incorrect surcharge calculation.

Filing the form without checking if it's an amended return also leads to complications. If corrections are necessary after initial submission, the box indicating an amended return must be checked to alert the Department of Revenue to the revision. Failing to do so can cause confusion and delays in processing.

There is also the mistake of neglecting to include the confirmation number for online payments. If payment is made online, this confirmation number provides proof of payment and should be included on the form. Omitting this information might result in unrecognized payments.

Incorrectly filling out the principal officer’s and preparer's information sections with incomplete or inaccurate details can also result in processing delays. The signature, print name, title, telephone number, and email address of both the principal officer and the preparer are critical for verification and communication purposes.

Forgetting to calculate penalties and interest correctly is another oversight. If the form or payment is submitted late, additional charges apply. The specifics for calculating these amounts are provided on the form, but they are often overlooked or misunderstood, leading to incorrect totals on lines 5 and 6.

By paying close attention to these details, individuals can avoid common mistakes and ensure their Kentucky 74A118 forms are accurately completed and duly processed.

When dealing with the Kentucky 74A118 form, commonly used for Monthly Insurance Surcharge Reports, several other forms and documents are often required to complete insurance-related reporting and compliance. These additional documents assist in ensuring the accuracy and completeness of the information provided to the Kentucky Department of Revenue and other regulatory bodies.

These documents play a significant role in the regulatory and compliance procedures for insurance providers operating in Kentucky. From providing evidence of insurance coverage to correcting previously submitted information and ensuring proper financial reporting, each document supports the overarching goal of transparency and compliance in the insurance industry. Understanding the purpose and requirements of these forms is crucial for any insurance provider to maintain good standing and comply with Kentucky state laws.

The Kentucky 74A118 form, focused on insurance surcharge reporting, shares functional and operational similarities with several other types of regulatory reporting forms across the United States. One such similarity can be found in the New York Quarterly Insurance Premium Tax Form, which requires insurers to report and pay taxes on premiums collected. Both forms serve as a means for state governments to collect taxes or surcharges on insurance premiums, requiring detailed information about premiums collected, adjustments, and exemptions. They are crucial tools for ensuring compliance with state laws regarding insurance taxation.

Similarly, the California Insurance Tax Form, used by the California Department of Tax and Fee Administration, parallels the Kentucky 74A118 form in its purpose of collecting tax-related information from insurance companies. Both forms necessitate the declaration of total premiums collected within the state, detailing exempt premiums and calculating the amount due after adjustments. This ensures that both states maintain a steady revenue stream from the insurance sector, fostering a regulated insurance market.>

Another comparable document is the Texas Premium Tax Form, utilized by the Texas Department of Insurance. Like the Kentucky form, it mandates insurers to report premiums collected, allowing for certain exemptions and adjustments. Both documents play a vital role in the oversight of insurance companies, ensuring they contribute their fair share to state revenues. The structured approach to declaring premiums and calculating dues underlines the importance of transparency and accountability in the insurance industry.

Florida's Insurance Premium Taxes and Fees Return shares a similar foundation with Kentucky's 74A118 form, as both are designed to calculate and collect taxes or surcharges on insurance premiums. They require detailed reporting of all insurance transactions within the state, emphasize compliance with state laws, and support the financial integrity of the state’s insurance system. These forms act as a comprehensive tool for revenue departments to track and manage the collection of insurance-related payments.

Illinois's Insurance Premiums Tax Return is another document that echoes the functionalities of Kentucky's 74A118. Insurers in Illinois, like those in Kentucky, must report on premiums received, highlighting the necessity for companies to maintain meticulous records of their insurance transactions for accurate tax reporting. The emphasis on detailed reporting underscores the states' efforts to ensure a fair and efficient taxation system within the insurance sector.

The Pennsylvania Insurance Premium Tax Return also resembles the Kentucky 74A118 form, particularly in its focus on collecting state revenue from insurance operations. Both states require insurance entities to accurately report their earnings from premiums, adhering to a set of rules and regulations designed to standardize financial obligations across the insurance industry. This parallelism showcases the widespread approach to managing and regulating insurance taxation at the state level.

Similarly, New Jersey's Insurance Premium Tax form aligns with Kentucky’s approach, compelling insurance companies to submit detailed reports on their premium collections for tax purposes. Both forms serve as essential tools for the respective states in enforcing tax laws and regulations, ensuring that insurance companies contribute to the state's economy. The structured reporting requirements reflect the complexity and significance of the insurance market's role in state finances.

The Ohio Commercial Activity Tax (CAT) Return, while broader, shares a core similarity with Kentucky's form in terms of taxing business activities, including insurance. Insurance companies operating in Ohio must account for their premiums when calculating their CAT liability. This demonstrates the broader application of premium-based taxation beyond just the insurance sector, highlighting a unified approach towards taxation of business activities across different states.

These documents, each tailored to the specific requirements of their respective states, collectively illustrate the complexities and similarities in insurance taxation and regulatory reporting across the United States. Despite their variations, the underlying goal remains consistent: to ensure a well-regulated insurance market that contributes fairly to state revenues, promoting economic stability and public welfare.

Completing the Kentucky 74A118 Monthly Insurance Surcharge Report accurately and on time is vital for compliance with state laws. To assist in this process, here are several do's and don'ts to keep in mind:

Following these guidelines will help ensure that your reporting is compliant, reducing the risk of penalties and ensuring that your commitments to regulatory obligations are met punctually.

Understanding the Kentucky 74A118 form, which relates to the Monthly Insurance Surcharge Report, is crucial for insurers operating within the state. However, several misconceptions often cloud its proper interpretation and application. Addressing these misunderstandings can ensure compliance with state regulations and streamline the reporting process for insurance providers.

Misconception 1: All insurance premiums are subject to the surcharge. It's a common belief that every premium collected by an insurer in Kentucky is subject to the surcharge. However, the form clearly outlines various exemptions, such as premiums returned to policyholders for terminated policies, specific types of insurance like accident and health, federal insured crop and flood insurance, reinsurance, title insurance, and workers' compensation, among others. Additionally, premiums collected from certain entities, including the federal government, nonprofit institutions, and state or local government for specific property coverage, are also not subject to the surcharge.

Misconception 2: The surcharge rate is negotiable or variable. The surcharge rate, set at .018 of the premium amount subject to the surcharge, is a fixed rate determined by state law. Insurers and policyholders cannot negotiate this rate. It's applied uniformly across all premiums that fall under the surcharge's scope, ensuring a standard calculation method for all parties involved.

Misconception 3: Surcharge reports are only filed annually. While the Kentucky 74A118 form does allow insurers with an annual liability of less than $1,000 for each of the previous two calendar years to report on a calendar year basis, most insurers are required to file their surcharge reports monthly. Insurers must submit these reports by the 20th day of the month following the month in which the premiums were collected, highlighting the importance of maintaining regular and accurate monthly records.

Misconception 4: Only domestic insurers are required to file the surcharge report. The requirement to file the Kentucky 74A118 surcharge report applies to every domestic, foreign, and alien insurer operating within the state, except those exclusively dealing in life and health insurance. This broad applicability ensures that all insurers contributing to risks located in Kentucky adhere to the same reporting standards, fostering a level playing field within the insurance industry.

Clarifying these misconceptions can help insurers better navigate the complexities of the Kentucky 74A118 form and ensure compliance with the Kentucky Department of Revenue's requirements. By understanding the specific exemptions, rate application, reporting frequency, and applicability, insurers can streamline their reporting processes and avoid penalties for inaccuracies or omissions.

Filling out the Kentucky 74A118 Monthly Insurance Surcharge Report can seem like a daunting task, but understanding a few key points can help simplify the process. Here’s what you need to know:

It's crucial for insurers to accurately fill out the form and stay on top of monthly or annual filings to avoid penalties. Ensuring that you understand which premiums are subject to the surcharge, as well as the exemptions and deductions you're entitled to claim, can significantly impact the accuracy of your filing and the total surcharge due. Always double-check your calculations and keep a record of your filings for future reference.

Aoc Ru 004 - Outlines the mandatory $25.00 fee for both individual and organizational requests for court records.

Map 350 - Emphasizes the importance of identifying primary caregivers and their relationship to the Medicaid member.