Kentucky 765 PDF Template

Kentucky 765 PDF Template

The Kentucky 765 form is a pivotal document for partnerships operating within the state, serving as the annual income return that must be meticulously filled out and submitted to the Kentucky Department of Revenue. Starting with the basic information such as the date business commenced or qualified, it extends to intricate details including the number of partners, which necessitates the attachment of K-1s, the partnership’s NAICS business code number, and various identifying details like the Federal Employer Identification Number and Kentucky Withholding Account Number. Furthermore, it requires a comprehensive attachment of the federal return, underscoring the interconnectedness of federal and state tax obligations. Entities such as general partnerships, limited partnerships, limited liability companies, and limited liability partnerships are all required to navigate the form’s complexities. It also capably addresses specifics like sales and use tax permit numbers, differentiating between initial, final, and amended returns, and even diving deep into the financial intricacies with sections dedicated to income, deductions, credits, and other significant financial data. Equally important is the form’s utility in determining the partnership's compliance with state tax withholdings for nonresident partners, illuminating its role not just as a tax document but as a facilitator of cross-state tax regulation among partners. With penalties for perjury as a stern reminder of the legal obligations, the Kentucky 765 form encapsulates a broad spectrum of requirements aimed at ensuring accurate and lawful financial reporting by partnerships.

|

Form 765 |

|

KENTUCKY |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

42A765 |

PARTNERSHIP INCOM E RETURN |

|

|

|

|||

|

Departm ent of Revenue |

➤ Attach a complete copy of the federal return. |

|

|

|

|||

|

|

For calendar year 2004 or fiscal year |

|

|

|

2004 |

||

|

|

|

|

|

||||

A. Date business com m enced or |

|

|

|

|||||

|

|

|

|

|

||||

|

|

|

|

|

|

|||

|

qualified |

|

|

|

|

|

|

|

|

|

beginning _________________ |

, 2004, and ending __________________ , 2005. |

|

|

|||

|

|

|

|

|

|

|

|

|

B. |

Num ber of partners (attach |

Nam e |

|

|

|

E. |

Federal Em ployer |

|

|

|

|

|

|

|

|

Identification Num ber |

|

|

|

|

|

|

|

|

|

|

|

|

Num ber and street or P.O. box |

|

|

|

|

|

|

C. |

NAICS business code num ber |

|

|

|

F. |

Kentucky Withholding |

||

|

|

|

|

|||||

|

|

|

|

|

|

|

Account Num ber |

|

|

|

|

|

|

|

|

|

|

|

|

City, tow n or post office |

County |

State |

ZIP code |

|

|

|

D. |

Partnership telephone num ber |

G. |

Sales and Use Tax |

|||||

|

|

|

|

|||||

|

|

|

|

|

|

|

Perm it Num ber |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H. |

Check applicable boxes: |

Initial return |

Final return |

Am ended return |

|

|

|

|

|

I. |

Check type of entity: |

General partnership |

Lim ited partnership |

Lim ited liability com pany |

|

|

Lim ited liability partnership |

|

|

|

|

|

|

|

J. |

Are disregarded entities included in this return? |

Yes |

No |

|

|

If yes, attach a schedule listing nam e and federal identification num ber of the disregarded entity. |

|||

|

|

|

|

|

K.Qualified investm ent partnership (Check box only if you are a general partnership or a lim ited partnership that has been form ed as a qualified investm ent partnership.)

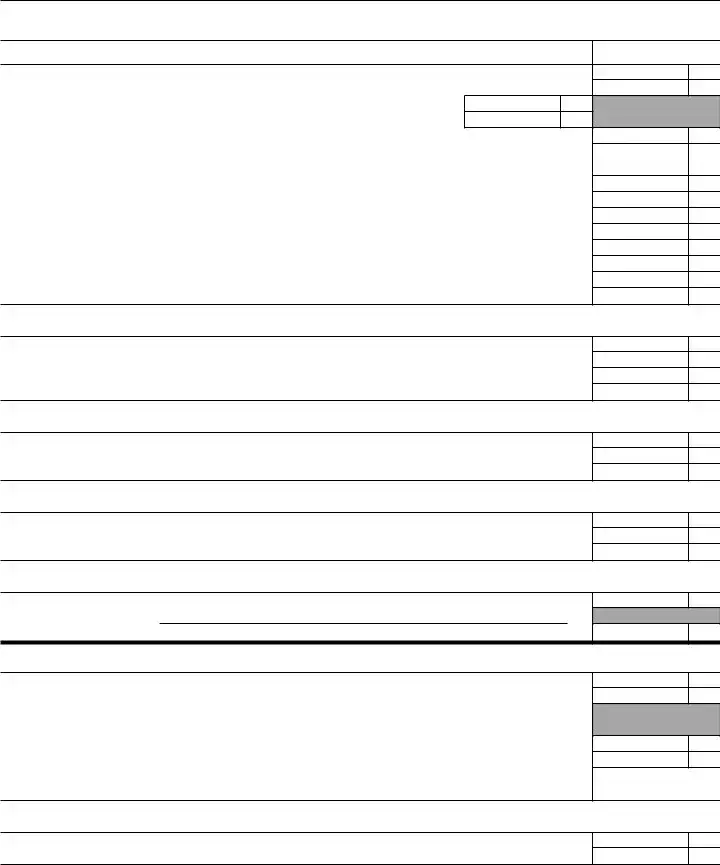

1. |

Federal ordinary incom e (loss) (Form 1065, line 22) |

1 |

2. |

Federal depreciation from Form 4562 |

2 |

3. |

Other (attach schedule) (see instructions) |

3 |

4. |

Total (add lines 1, 2 and 3) |

4 |

SUBTRACTIONS: |

|

|

5. |

Federal w ork opportunity credit |

5 |

6. |

Kentucky depreciation from revised Form 4562 |

6 |

7. |

Other (attach schedule) (see instructions) |

7 |

8. |

Total (add lines 5, 6 and 7) |

8 |

9. |

Ordinary income (loss) (line 4 less line 8) |

9 |

✍I declare under the penalties of perjury that this return (including any accom panying schedules and statem ents) has been exam ined by m e and, to the best of m y know ledge and belief, is a true, correct and com plete return.

Signature of partner or m em ber |

Identification num ber of partner or m em ber |

Date |

|

|

|

Typed or printed nam e of preparer other than taxpayer |

Identification num ber of preparer |

Date |

M ail to Kentucky Department of Revenue, Frankfort, Kentucky 40620.

Form 765 (2004) |

Page 2 |

|

|

Schedule

SECTION I

Income or (Loss)

|

|

(a) Distributive Share Items |

|

(b) Total Amount |

1. |

Ordinary incom e or (loss) from trade or business activities (page 1, line 9) |

................................................. |

1 |

|

2. |

Net incom e or (loss) from rental real estate activities (from attached federal schedule) |

2 |

||

3. |

a |

Gross incom e from other rental activities |

3a |

|

|

b |

M inus expenses (attach schedule) |

3b |

|

|

c |

Net incom e or (loss) from other rental activities |

3c |

|

4. |

Portfolio incom e or (loss): |

|

|

|

|

a |

Interest incom e |

4a |

|

|

b |

Dividend incom e |

4b |

|

|

c |

Royalty incom e |

4c |

|

|

d |

Net |

4d |

|

|

e |

Net |

4e |

|

|

f |

Other portfolio incom e or (loss) (attach schedule) |

4f |

|

5. |

Guaranteed paym ents to partners |

5 |

||

6. |

Net gain or (loss) under IRC Section 1231 (other than due to casualty or theft) (attach federal Form 4797) 6 |

|||

7. |

Other incom e or (loss) (attach schedule) |

7 |

||

Deductions |

|

|

||

8. |

Charitable contributions (attach list) and housing for hom eless deduction (attach Schedule HH) |

8 |

||

9. |

IRC Section 179 expense deduction (attach federal Form 4562 and Kentucky revised Form 4562) |

9 |

||

10. Deductions related to portfolio incom e (do not include investm ent interest expense) |

10 |

|||

11. |

Other deductions (attach schedule) |

11 |

||

Investment Interest |

|

|

||

12. |

a Interest expense on investm ent debts |

12a |

||

|

b |

(1) Investm ent incom e included on lines 4a, 4b, 4c and 4f above |

12b(1) |

|

|

|

(2) Investm ent expenses included on line 10 above |

12b(2) |

|

Credits |

|

|

|

|

13. Kentucky Unem ploym ent Tax Credit (attach Schedule UTC) |

13 |

|||

14. Recycling and Com posting Equipm ent Tax Credit (attach approved Schedule RC) |

14 |

|||

15. |

Other (see instructions) ➤ |

..................... |

15 |

|

Other |

|

|

|

|

16. |

a Total expenditures to w hich IRC Section 59(e)(2) election m ay apply |

16a |

||

|

b |

Type of expenditures |

|

16b |

17. Other item s and am ounts not reported above (attach schedule) |

17 |

|||

SECTION |

|

|

||

1. |

Partnership’s Kentucky property and payroll |

1 |

2. |

Partnership’s total property and payroll |

2 |

If line 1 is equal to line 2, enter 100 percent on Schedule

3. |

Partnership’s Kentucky gross receipts |

3 |

4. |

Partnership’s total gross receipts |

4 |

5. |

Nonresident partner’s taxable percentage (line 3 divided by line 4). Enter the percentage on |

|

|

Schedule |

5 |

%

SECTION

1. |

Individual nonresident partners' net distributive share of taxable incom e |

1 |

2. |

Individual nonresident partners' net distributive share w ithheld |

2 |

| Fact | Detail |

|---|---|

| Form Type | Kentucky Form 765 is a Partnership Income Return form. |

| Governing Law | This form is governed by Kentucky state law and regulations pertaining to income taxation of partnerships. |

| Submission Requirement | A complete copy of the federal return must be attached upon submission. |

| Applicable Period | For the calendar or fiscal year beginning in 2004 and ending in 2005. |

| Key Information Needed | Information such as the number of partners, NAICS business code number, Federal Employer Identification Number, and Kentucky Withholding Account Number are required. |

| Special Indications | The form allows for the indication of special circumstances such as initial, final, or amended returns, and if it’s for a general partnership, limited partnership, limited liability company, or limited liability partnership. |

Filling out the Kentucky 765 form is a necessary procedure for partnerships that need to report their income return to the Kentucky Department of Revenue. This task requires attention to detail and accuracy to ensure compliance with tax regulations. The Kentucky 765 form consists of several sections that collect information about the partnership's income, deductions, partners' shares, and more. Once completed, this form, along with any schedules and attachments, should be sent to the Kentucky Department of Revenue. Here is a step-by-step guide to help you fill out the form correctly.

Once the Kentucky 765 form is submitted, the Kentucky Department of Revenue will review the provided information. Depending on the complexity of the return and current processing times, it may take several weeks for the form to be processed. It is crucial to retain copies of all documents submitted for your records and future reference.

What is the purpose of the Kentucky 765 form?

The Kentucky 765 form serves as the income return document for partnerships operating within the state of Kentucky. It's designed to report earnings, deductions, credits, and other pertinent financial information associated with the partnership for the calendar or fiscal year specified. Additionally, the form plays a crucial role in detailing each partner's share of income, deductions, and credits through attached schedules. Partnerships are also required to attach a complete copy of their federal return, ensuring that both state and federal tax obligations are aligned and transparent.

Who needs to file the Kentucky 765 form?

This form must be filed by entities recognized as partnerships under Kentucky law. This includes general partnerships, limited partnerships, limited liability companies (LLCs) that are treated as partnerships for tax purposes, and limited liability partnerships (LLPs). If a partnership has income, deductions, or credits that flow through to its partners, it needs to complete and submit Form 765. Importantly, if disregarded entities are part of the partnership, a schedule listing each disregarded entity's name and federal identification number must be attached, indicating the form's comprehensive approach to capturing the tax responsibilities of complex partnership structures.

How does a partnership report its income and deductions on the Kentucky 765 form?

Income and deductions are reported in a detailed manner on the Kentucky 765 form. The form requires information such as federal ordinary income or loss, federal and Kentucky depreciation, and other income or deductions that can affect the partnership's taxable income. This information is summarized in the initial sections of the form, with subsequent schedules (Schedule K) breaking down each partner's distributive share of income, deductions, and credits. These distributions are based on the partnership's agreed-upon allocations. It’s essential for partnerships to accurately report both their total earnings and the associated deductions to determine their tax obligations accurately.

What is the process for calculating nonresident partner's taxable percentage?

The Kentucky 765 form includes a section dedicated to computing the taxable percentage for nonresident partners. This calculation begins by comparing the partnership's Kentucky-based property and payroll against its total property and payroll. If the partnership operates entirely within Kentucky, this percentage is 100%. However, if the partnership operates both in and out of Kentucky, the form guides the preparer through a series of steps to determine the proportion of the partnership's gross receipts from Kentucky. This percentage then dictates the nonresident partner's taxable share, reflecting the degree to which their income is attributable to sources within Kentucky. This process ensures that nonresident partners are taxed appropriately for income derived from the state.

Filling out the Kentucky 765 form, which is the Partnership Income Return form, can be tricky. Certain common mistakes can lead to errors in the submission. Being aware of these can save time and prevent potential issues with tax returns.

One of the primary oversights involves failing to attach a complete copy of the federal return. The Kentucky 765 form mandates that partnerships include their entire federal return. This requirement is crucial for verifying the income and deductions reported at the state level.

Incorrectly listing the number of partners and not attaching the necessary K-1s is another frequent mistake. The form requires accurate reporting of all partners within the business, and each must have their corresponding Schedule K-1 attached. This schedule outlines each partner's share of the income, deductions, and credits.

Another error involves miscalculations in the income sections, including federal ordinary income (loss), federal depreciation, and adjustments. Accurate entry in these sections is critical for determining the correct taxable income for the partnership.

Understanding and avoiding these common mistakes can streamline the process of filling out the Kentucky 765 form, ensuring a smoother, error-free submission.

When completing the Kentucky 765 form, a variety of other documents and forms may be needed to ensure a thorough and compliant partnership income return. Understanding these additional forms will help partners navigate the tax filing process more effectively, ensuring that all necessary information is accurately reported to the Kentucky Department of Revenue.

Utilizing these forms in conjunction with the Kentucky 765 ensures that both the partnership and its partners are reporting their income and deductions correctly to the IRS and Kentucky Department of Revenue. Keeping accurate and comprehensive records, along with timely submission of all required forms, helps in minimizing tax liabilities and avoiding potential penalties.

The United States federal Form 1065, Partnership Income Tax Return, closely resembles Kentucky's Form 765 in its purpose and content. Both serve partnerships needing to report their income, deductions, and the distribution of shares to their partners. Each form requires the partnership to attach a copy of the other financial documents, like depreciation schedules and K-1 forms, to provide a comprehensive account of the fiscal activities. Where Form 1065 addresses federal requirements, Form 765 satisfies Kentucky's state-specific stipulations, making them parallel tools for tax reporting at different governmental levels.

Form 4562, Depreciation and Amortization, is cited in both the federal Form 1065 and Kentucky's Form 765, underlining their similarity in demanding detailed accounts of depreciation expenses. These forms necessitate a precise enumeration of assets, the calculation of depreciation for tax purposes, and adjustments specific to respective jurisdictions. The inclusion of Form 4562 in the documentation process highlights the shared requirement for businesses to systematically report the depreciation of their assets, facilitating a uniform approach to tracking the declining value of business investments over time.

Kentucky's Schedule K-1 (Form 765) mirrors the federal Schedule K-1 (Form 1065) in its utility and function. Both are designed to report the share of income, deductions, credits, etc., passed through to partners or members of partnerships or limited liability companies treated as partnerships for tax purposes. They ensure that the income earned and taxes paid at the partnership level are accurately reported and allocated to the individual partners, so they can report their shares on personal tax returns, thereby seamlessly linking partnership activities with individual tax liabilities.

The Kentucky Department of Revenue Form 720, the Corporation Income Tax Return, and Form 765 share a fundamental similarity in their roles as state-level tax documents catering to different business structures – corporations vs. partnerships. They both demand detailed financial reporting, including income, deductions, and tax calculations pertinent to their respective entities. While their specific formats and requirements reflect the unique characteristics of the entities they serve, the overarching goal to report and calculate Kentucky state tax liabilities unites them.

The IRS Form 4797, Sales of Business Property, is similar to sections within Kentucky's Form 765 that deal with the reporting of gains or losses from the sale of assets used in a business. Both require detailed information about the sale or exchange of property and play a pivotal role in adjusting the income subject to taxation, reflecting the interconnectedness of asset disposition and taxable income for businesses. This common feature underscores the necessity for businesses to account for and report significant changes in their asset bases for tax purposes.

Form 4562, Kentucky's counterpart for reporting depreciation adjustments specific to state tax codes, shares its framework and intent with the federal Form 4562, underscoring its relevance in both federal and state tax preparations. This similarity highlights the intricate relationship between depreciable asset reporting and tax liability adjustments, catering to the nuanced modifications that state-level considerations infuse into the broader, nationally standardized depreciation calculations.

IRS Form 1065-B, U.S. Return of Income for Electing Large Partnerships, parallels Kentucky's Form 765 in targeting a specialized subset of partnerships – those that are large and elect out of certain standard treatment. Although specific in their focus, both forms mandate comprehensive disclosures of income, gains, losses, deductions, and credits, reflecting the enhanced reporting obligations incumbent upon larger partnerships. These forms reflect the heightened complexity and scrutiny directed at large partnership entities across both federal and state tax landscapes.

Kentury Schedule UTC, Unemployment Tax Credit, which may accompany Form 765, is akin to various federal incentives aimed at encouraging specific business behaviors, like the Federal Work Opportunity Credit. Each is designed to alleviate the tax burden on businesses contributing positively to broader economic or social goals, such as employment growth. By providing detailed mechanisms for claiming these benefits, both Kentucky and the federal government align on the principle of using tax policy to incentivize beneficial business practices.

The Recycling and Composting Equipment Tax Credit Schedule, attachable to Kentucky Form 765, demonstrates a targeted approach to environmental stewardship through tax incentives, a concept mirrored in various federal tax credits aimed at promoting sustainability. These pieces of the tax code encourage investments in environmentally friendly practices by offering financial benefits for compliance, illustrating the shared use of tax policies to drive investment in priority areas across different levels of governance.

The form for the IRC Section 179 expense deduction, required alongside both federal and Kentucky tax returns for businesses, illustrates the alignment in taxing authorities' efforts to stimulate business investment in machinery and equipment. By allowing upfront deductions of such purchases, both the IRS and the Kentucky Department of Revenue aim to lower the fiscal barrier to capital investment, fostering an environment conducive to business growth and modernization, underscoring their shared focus on economic development through tax policy.

When preparing the Kentucky 765 form, a Partnership Income Return, paying attention to detail and accuracy is imperative for compliance. Below is a comprehensive list of practices to follow and to avoid, ensuring the process is carried out efficiently and effectively.

Compliance with these guidelines ensures the Kentucky 765 form is submitted accurately and efficiently, minimizing errors and potential for audit. Always consult with a professional if unsure about any requirements or procedures.

The Kentucky 765 form is an essential document for partnerships conducting business within Kentucky, serving as the partnership income return. Despite its significance, there are several misconceptions surrounding this form that can lead to confusion for businesses. Here, we aim to clarify these misunderstandings and provide a clearer understanding of the form and its requirements.

This is incorrect. The instructions clearly state that a complete copy of the federal return must be attached when submitting the Kentucky 765 Form. This is crucial for ensuring that all information is consistent across both federal and state filings.

Even partnerships without a physical presence may be required to file if they derive income from sources within Kentucky. The nexus laws often consider income sourced to the state as a valid reason for filing requirements.

While income reporting is a significant part of the form, Form 765 also requires the disclosure of partners' shares of income, credits, and deductions. It provides a comprehensive report on the partnership's financial activities in Kentucky.

Actually, the form only needs to be signed by one partner or member who declares that the return, including any accompanying schedules and statements, has been examined and is true, correct, and complete to the best of their knowledge.

On the contrary, significant events such as the commencement of the partnership, any amendments, or the final return indicate critical stages in the partnership's lifecycle that must be reported accurately on the form.

This is not true. If disregarded entities are included in the return, a separate schedule listing the name and federal identification number of the disregarded entity must be attached, indicating the requirement for transparency regarding all entities involved.

Filing procedures and requirements can evolve, reflecting changes in tax laws or administrative practices. Always refer to the most current form and instructions to ensure compliance with the latest requirements.

Understanding these misconceptions and how they differ from the reality of the form's requirements can help partnerships navigate their tax obligations more efficiently and avoid potential penalties for non-compliance. The Kentucky 765 form plays a crucial role in tax administration for partnerships and getting it right is essential for business operations within the state.

When dealing with the Kentucky 765 form, which is the income return for partnerships, there are several critical points to consider. These key takeaways will guide you through the process of accurately filling out and using the form.

Attach a complete copy of the federal return: It's mandatory to include the entire federal return with the Kentucky 765 form. This ensures consistency and completeness of the financial information being reported.

Specify the reporting period: Clearly indicate the beginning and ending dates for the tax year or fiscal year the return covers. This is crucial for the Department of Revenue to match your return to the correct tax period.

The number of partners and their information, including K-1s, must be accurately included. Each partner's share of income, deductions, and credits is reported on these K-1 forms and must align with the totals on the Kentucky 765 form.

Enter all identification numbers correctly, such as the Federal Employer Identification Number and the Kentucky Withholding Account Number. Mistakes in these numbers can lead to processing delays or issues with your return.

If applicable, check the correct boxes for the type of entity and if you're filing an initial, final, or amended return. This information helps the Department of Revenue understand the context of your submission.

For partnerships with nonresident partners, pay special attention to the Computation of Nonresident Partner's Taxable Percentage and the Amount Withheld on Individual Nonresident Partners sections. Getting these calculations right is imperative for complying with state withholding requirements.

Don’t overlook deductions and credits, such as the Kentucky depreciation and Work Opportunity Credit. Properly claiming these can significantly impact the partnership's taxable income.

Ensure accuracy and completeness: All schedules and additional documentation, such as revised Form 4562 for Kentucky depreciation or Schedule RC for Recycling and Composting Equipment Tax Credit, should be attached if relevant. Also, thoroughly review the form before submission to avoid errors that could delay processing.

Compliance with these guidelines not only ensures the accurate and timely processing of the Kentucky 765 form but also helps in avoiding potential penalties for incorrect or incomplete filings.

Aoc Ru 004 - Details on how to request your own court record or someone else's, with a standardized $25.00 processing fee.

Aoc-856 - Designed for annual or biennial submission, depending on the estate's net worth, to ensure transparency and accountability.

Kyu Tax Filing - Advisory to keep the instructions on page 1 while submitting page 2 instills clarity and aids in the correct completion of the KY Weight Distance form.