Kentucky Tax Requisition PDF Template

Kentucky Tax Requisition PDF Template

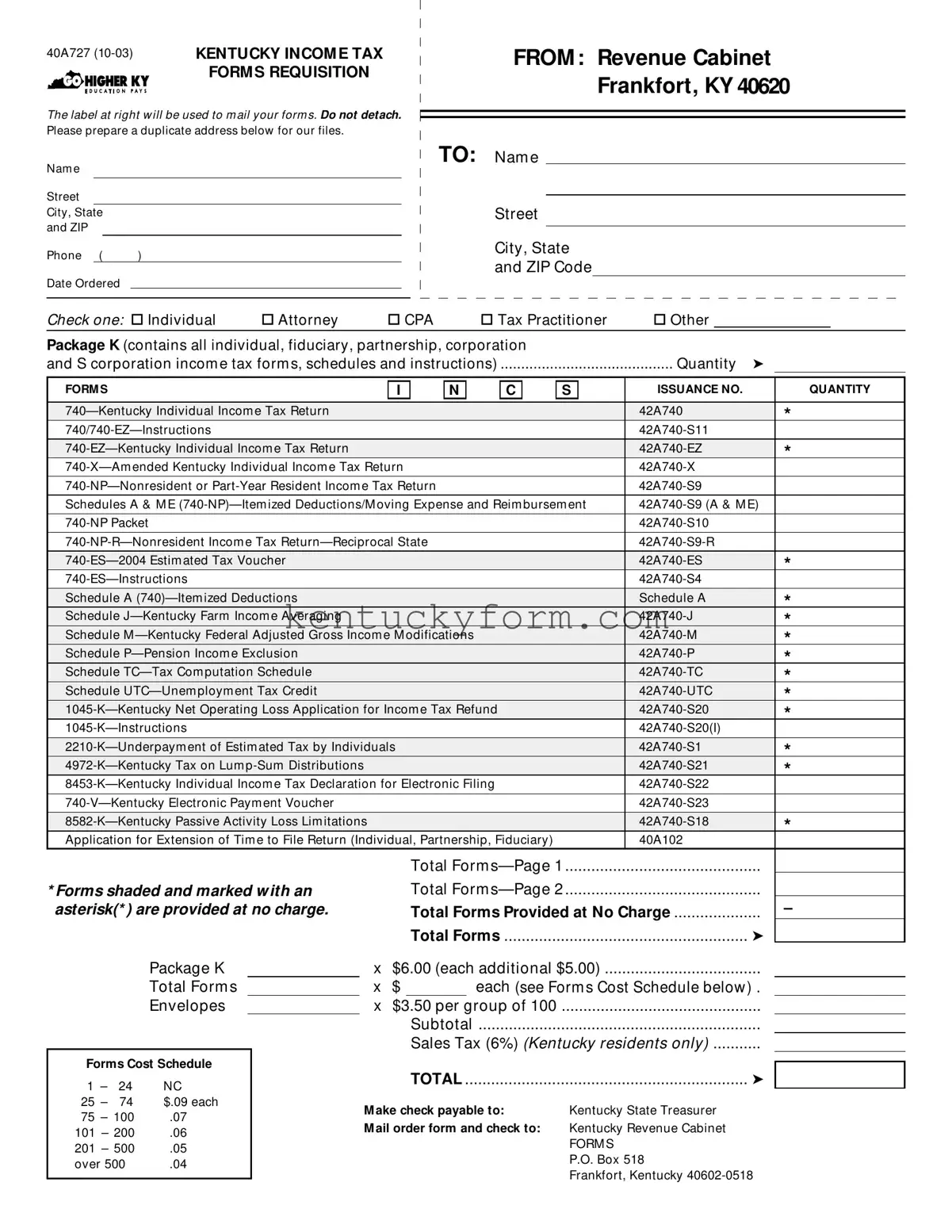

At the heart of Kentucky's tax filing process lies the Kentucky Tax Requisition form, a pivotal document ensuring that individuals and entities obtain the necessary forms for filing their income taxes. This form, identified by its form number 40A727, is crafted to streamline the acquisition of various tax-related documents directly from the Revenue Cabinet in Frankfort, KY. Tailored to meet the diverse needs of filers, it caters not only to individuals but also to attorneys, certified public accountants (CPAs), tax practitioners, and others engaged in the preparation of tax documents. One of the form's distinctive features is the inclusion of Package K, which compiles all essential forms and instructions required for filing individual, fiduciary, partnership, corporation, and S corporation income taxes. Additionally, it meticulously lists forms for specific needs such as the Kentucky Individual Income Tax Return, amended returns, nonresident or part-year resident income tax returns, estimated tax vouchers, and various schedules for itemized deductions, modifications, and tax computation, underscoring its comprehensive nature. The requisition process is augmented with a structured pricing scheme for ordering forms, highlighting the state's commitment to accessibility and efficiency. Moreover, the encouragement of electronic filing by the Kentucky Revenue Cabinet through this form signifies a push towards leveraging technology for a more streamlined and efficient tax filing experience, reflecting modern trends in tax administration.

40A727 |

KENTUCKY INCOM E TAX |

|

|

|

FORM S REQUISITION |

|

|

|

|

|

|

The label at right w ill be used to m ail your form s. Do not detach.

Please prepare a duplicate address below for our files.

FROM : Revenue Cabinet Frankfort, KY 40620

Nam e

Street

City, State

and ZIP

TO: Nam e

Street

Phone ( |

) |

|

|

|

|

Date Ordered

City, State and ZIP Code

Check one: ο Individual |

ο Attorney |

|

ο CPA |

ο Tax Practitioner |

ο Other |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Package K (contains all individual, fiduciary, partnership, corporation |

|

|

|

|

|

|

|

|||||||||||

and S corporation incom e tax form s, schedules and instructions) |

|

Quantity |

➤ |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FORM S |

|

|

|

I |

|

|

N |

|

|

C |

|

S |

|

ISSUANCE NO. |

|

QUANTITY |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

42A740 |

|

* |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Schedules A & M E |

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule A |

|

|

|

|

|

|

|

|

|

|

|

Schedule A |

|

* |

|

|||

Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|||||

Schedule M |

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

* |

|

|||||||||||

Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|||||

Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|||||

Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|||||

|

|

|

|

|||||||||||||||

|

|

|

* |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

* |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|||||

|

|

|

|

|||||||||||||||

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|||||

Application for Extension of Tim e to File Return (Individual, Partnership, Fiduciary) |

|

|

40A102 |

|

|

|||||||||||||

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

Total Form |

|

|

|

|

|

|||||||

* Forms shaded and marked w ith an |

|

|

|

.............................................Total Form |

|

|

|

|

|

|||||||||

asterisk(* ) are provided at no charge. |

|

|

|

Total Forms Provided at No Charge |

– |

|||||||||||||

|

|

|

|

|

|

........................................................Total Forms |

|

|

|

➤ |

|

|

||||||

Package K |

|

|

x |

....................................$6.00 (each additional $5.00) |

|

|

|

|

|

|||||||||

Total Form s |

|

|

x |

$ |

|

|

|

|

each (see Form s Cost Schedule below ) . |

|

||||||||

Envelopes |

|

|

x $3.50 per group of 100 |

.............................................. |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

Subtotal |

................................................................. |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

...........Sales Tax (6%) (Kentucky residents only) |

|

|

||||||||||

Forms Cost Schedule

1 – |

24 |

NC |

|

25 |

– |

74 |

$.09 each |

75 |

– 100 |

.07 |

|

101 |

– 200 |

.06 |

|

201 |

– 500 |

.05 |

|

over 500 |

.04 |

||

TOTAL |

➤ |

M ake check payable to: |

Kentucky State Treasurer |

M ail order form and check to: |

Kentucky Revenue Cabinet |

|

FORM S |

|

P.O. Box 518 |

|

Frankfort, Kentucky |

FORM S |

ISSUANCE NO. |

|

|

QUANTITY |

Kentucky Individual Incom e Tax Installm ent Agreem ent Request |

12A200 |

|

|

|

42A741 |

|

|

|

|

42A741(I) |

|

|

|

|

|

|

|

||

Schedule |

42A741 |

|

|

|

42A765 |

|

|

|

|

42A765(I) |

|

|

|

|

Schedule |

42A765 |

|

|

|

41A720 |

|

* |

||

41A720(I) |

|

|||

|

|

|

||

41A720S |

|

* |

||

41A720S(I) |

|

|||

|

|

|

||

Schedule |

41A720S |

|

* |

|

41A720X |

|

|||

|

|

|

||

41A720ES |

|

|

* |

|

|

|

|||

|

|

|

||

Schedule A |

41A720A |

|

* |

|

Application for Extension of Tim e to File KY Corporation Incom e and License Tax Return |

41A720SL |

|

||

|

* |

|||

Schedule |

41A720EZC |

|

||

|

* |

|||

Schedule |

41A720HH |

|

||

|

* |

|||

Schedule |

41A720RC |

|

||

|

* |

|||

Schedule |

41A720RC(C) |

|

||

|

* |

|||

Schedule RC |

41A720RC |

|

||

|

* |

|||

41A722 |

|

|||

|

* |

|||

|

||||

|

* |

|||

Total |

|

➤ |

||

|

|

|||

|

|

|

|

|

ENVELOPES (Available in groups of 100 only) |

|

|

|

|

Refund 6" x 9" Blue |

|

➤ |

|

|

Paym ent 6" x 9" Yellow |

|

➤ |

|

|

* Forms shaded and marked w ith an asterisk(* ) are provided at no charge.

Electronic

‰Federal/State Electronic Filing Federal/State Online Filing

Have you seen our Web page?

Form s

‰Instructions

and a Whole Lot M ore!

w w w.revenue.ky.gov

| Fact Number | Description |

|---|---|

| 1 | The Kentucky Tax Requisition form, labeled 40A727, is used for ordering various state income tax forms and instructions. |

| 2 | Orders can be placed by individuals, attorneys, CPAs, tax practitioners, or others needing access to Kentucky income tax forms. |

| 3 | Package K includes all individual, fiduciary, partnership, corporation, and S corporation income tax forms, along with schedules and instructions. |

| 4 | Fees for ordering documents through this form are based on the quantity ordered, with a detailed cost schedule provided for quantities ranging from 1 to over 500 forms. |

| 5 | Certain forms and instructions, identified with an asterisk (*), are provided at no charge. |

| 6 | Payments for orders from the Kentucky Tax Requisition form are to be made to the Kentucky State Treasurer. |

| 7 | The governing law for the requisition and distribution of Kentucky income tax forms is under the jurisdiction of the Kentucky Revenue Cabinet, based in Frankford, KY. |

Upon deciding to request Kentucky tax forms, one should prepare to navigate the requisition process with care. This involves clearly identifying the type of forms needed, whether for individual use, professional services (such as those provided by attorneys, CPAs, or tax practitioners), or perhaps another category. The Kentucky Tax Requisition Form allows users to order various tax documents, including income tax returns, estimated tax vouchers, and specific schedules related to deductions or credits. It's crucial to specify the quantity of each form alongside providing accurate address information for where the forms should be sent. Following a methodical approach ensures that all necessary materials are received promptly for tax preparation purposes.

With the form accurately filled out and sent, the requested tax forms should arrive at the provided address, enabling the completion of tax-related tasks. It's essential to consider timing when placing an order, ensuring there's ample room before any deadlines for preparing and submitting taxes.

What is the purpose of the Kentucky Tax Requisition form?

The purpose of the Kentucky Tax Requisition form, labeled 40A727, is to enable individuals, attorneys, CPAs, tax practitioners, and others to order various types of income tax forms and related schedules and instructions. These forms are necessary for filing individual, fiduciary, partnership, corporation, and S corporation income tax returns in the state of Kentucky. This form facilitates the ordering process by listing all available forms and their respective quantities, as well as providing a cost schedule for bulk orders.

Who can use the Kentucky Tax Requisition form?

The Kentucky Tax Requisition form can be used by a broad category of requesters including individuals, attorneys, Certified Public Accountants (CPAs), tax practitioners, and others who may need Kentucky income tax forms for filing purposes. The form allows these users to select the specific types of tax forms they require, such as individual income tax returns, nonresident or part-year resident income tax returns, estimated tax vouchers, and more, depending on their particular filing needs.

How are the forms priced, and is there a charge for all forms ordered using the Kentucky Tax Requisition form?

Not all forms ordered using the Kentucky Tax Requisition form are subject to a charge. Forms marked with an asterisk (*) are provided at no charge. For forms that do incur a cost, the pricing structure is based on the quantity ordered. The cost per form decreases as the quantity increases, according to the following schedule:

Additionally, there is a charge for envelopes if they are ordered, priced at $3.50 per group of 100. Kentucky residents are also subject to a 6% sales tax on their orders.

How do you submit the Kentucky Tax Requisition form, and what are the payment options?

To submit the Kentucky Tax Requisition form, complete the necessary information, including the quantity and type of forms needed, and the total cost calculation based on the forms and quantities ordered. Once completed, a check made payable to the Kentucky State Treasurer should accompany the form. Both the order form and the check should then be mailed to the Kentucky Revenue Cabinet, FORMS P.O. Box 518, Frankfort, Kentucky, 40602-0518.

Are there any alternatives to ordering tax forms via the Kentucky Tax Requisition form?

Yes, there are alternatives to ordering tax forms through the Kentucky Tax Requisition form. One significant alternative is electronic filing, which the form itself promotes as advantageous. Taxpayers can choose either federal/state electronic filing or federal/state online filing, both of which may eliminate the need for physical forms. Additionally, the Kentucky Revenue website offers forms, instructions, and more resources that can be accessed digitally, providing a convenient alternative to manual ordering and reducing paper usage.

Filling out the Kentucky Tax Requisition form can seem straightforward, but common mistakes often lead to processing delays or incorrect tax form shipments. Being aware of these pitfalls can save both time and frustration.

The first mistake to avoid is failing to mark the correct requester category. Whether Individual, Attorney, CPA, Tax Practitioner, or Other, this selection guides the Kentucky Revenue Cabinet on the type of forms and instructions to provide.

Another error happens when requesters overlook the quantity section. It might seem minor, but incorrectly specifying the number of forms needed results in receiving too few or too many, impacting both the requester and inventory levels at the Revenue Cabinet.

It's also important to double-check the form numbers and descriptions. For example, ordering form 42A740 for individual returns when needing 42A740-NP for nonresident or part-year residents can cause unnecessary back-and-forth and delay tax filing.

In sum, carefully filling out the Kentucky Tax Requisition form, paying close attention to details and requirements, can prevent delays and ensure you receive the correct tax forms promptly. Always verify your entries and calculations before submission.

When handling tax matters in Kentucky, especially with the Kentucky Tax Requisition form, individuals and businesses may find themselves in need of several other forms and documents to complete their financial and tax-related responsibilities accurately. These forms are essential for various purposes, such as reporting income, making amendments to previously filed returns, estimating upcoming taxes, and seeking extensions for filing. Here are six notable documents often used together with the Kentucky Tax Requisition form, each serving a unique role in the tax preparation and filing process.

These documents, in conjunction with the Kentucky Tax Requisition form, are critical tools for managing tax affairs in Kentucky efficiently. They ensure compliance with state tax laws while providing various options for taxpayers to report income, settle liabilities, and keep accurate financial records. Providing the correct information on these forms is crucial for the smooth processing of tax-related matters and for avoiding possible penalties for inaccuracies or omissions.

The IRS Form 1040, similar to the Kentucky 740—Kentucky Individual Income Tax Return, serves as the standard federal income tax form for individuals. Both forms are designed to calculate the tax owed or refund due to the taxpayer and include sections for reporting income, deductions, and tax credits. However, while the Kentucky 740 form focuses on state tax obligations, the IRS Form 1040 addresses federal tax requirements.

Form W-4, known as the Employee's Withholding Certificate, shares similarities with the Kentucky 740-ES—2004 Estimated Tax Voucher. Both forms involve the estimation and adjustment of taxes paid throughout the year. The Kentucky 740-ES helps individuals estimate state taxes due, facilitating proper quarterly payments, whereas the Form W-4 assists employers in withholding the correct federal income tax from employees' paychecks.

The IRS Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return, parallels the Application for Extension of Time to File Return found within the Kentucky Tax Requisition form package. Each form provides individuals the means to request additional time to file their respective tax returns—Form 4869 at the federal level and the state form for Kentucky filers—though neither extends the time for tax payment.

The Schedule K-1 forms within the IRS and Kentucky tax frameworks serve analogous purposes but in different contexts. The Kentucky Schedule K-1 (741) and (765) allocations are akin to the federal Schedule K-1 forms for partnerships, S corporations, and trusts, detailing a beneficiary's share of income, deductions, and credits. This arrangement ensures transparency in reporting pass-through entities' income on individual tax returns.

Form 8822, Change of Address, issued by the IRS, corresponds to the administrative process implied by the Kentucky Tax Requisition form for updating taxpayer contact information. While the Kentucky form indirectly facilitates updating addresses through the ordering of tax forms, IRS Form 8822 directly updates taxpayer records with the federal government to ensure accurate correspondence delivery.

IRS Form 1120, U.S. Corporation Income Tax Return, aligns with the Kentucky 720—Kentucky Corporation Income and License Tax Return in its function to report corporate income taxes. Each form is tailored to its respective tax authority's requirements, with Form 1120 catering to federal tax obligations and the Kentucky 720 addressing the state's corporate tax structure.

IRS Form 7004, Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns, finds its counterpart in the Kentucky Application for Extension of Time to File KY Corporation Income and License Tax Return. Though one is for federal purposes and the other for state, both forms serve the crucial role of granting businesses additional time to compile and file detailed tax documents.

The IRS Form 2553, Election by a Small Business Corporation, has similarities with the Kentucky 720S—Kentucky S Corporation Income and License Tax Return and related schedules in terms of facilitating S corporation tax status. While Form 2553 is used to elect S corporation status at the federal level, the Kentucky 720S documents and their schedules manage the state-level tax implications of such an election, including income, deductions, and credit allocations among shareholders.

Form 9465, IRS Installment Agreement Request, is comparable to the Kentucky Individual Income Tax Installment Agreement Request form. Both exist to assist taxpayers in setting up payment plans for outstanding tax liabilities, providing a structured approach to settling debts over time with their respective tax authorities.

Lastly, the IRS Form 1045, Application for Tentative Refund, relates to the 1045-K—Kentucky Net Operating Loss Application for Income Tax Refund in its framework for managing losses. Each form allows for the carryback of net operating losses (NOLs), enabling taxpayers to amend previous years’ returns with current losses to secure potential refunds. The key difference is the jurisdiction in which the forms apply, with the IRS form addressing federal tax situations and the Kentucky form handling state tax matters.

Filling out the Kentucky Tax Requisition form accurately is crucial to ensure that your tax documents are correctly processed. Here are seven things you should do, along with seven things you shouldn't do, when completing this form.

Do:

Don't:

When it comes to filling out tax forms, it's easy to get tangled in a web of misinformation, especially with the Kentucky Tax Requisition form. Let's clear the air on some common misconceptions:

It's only for individuals. Many believe that the Kentucky Tax Requisition form is strictly for personal use. However, it’s also available for attorneys, CPAs, tax practitioners, and others managing taxes for a myriad of entities.

Everything will cost you. It's often assumed that all tax forms come with a fee. In reality, several forms, including key individual and corporate tax return documents, are provided at no charge.

You must know exactly what you need beforehand. While it helps to know what forms you need, the Package K option is there for those who need a comprehensive set of forms covering various tax situations.

Electronic filing options are limited. Some think Kentucky doesn’t support much electronic filing. However, electronic options are indeed available and encouraged, offering an easier and faster way to handle your tax submissions.

Special envelopes aren't important. Many underestimate the importance of ordering the correct envelopes. Kentucky provides specific envelopes for refunds and payments to streamline processing.

The process is only for Kentucky residents. While the form is primarily used by Kentucky residents, there are provisions for nonresidents or part-year residents to comply with their tax obligations in Kentucky.

You can only order forms by mail. While mailing is an option, Kentucky’s Revenue Cabinet also supports online form requests, making it more convenient for everyone involved.

Amended returns are a hassle. There’s a misconception that amending a return is cumbersome. Kentucky provides a specific form, 740-X, for this purpose, simplifying the process of correcting your tax return.

Estimates are guesswork. Many dread estimated tax vouchers, thinking they must blindly guess amounts. However, Kentucky offers a form and instructions to help calculate estimated taxes more accurately.

Assistance is hard to come by. The idea that finding help for filling out the requisition form is difficult is unfounded. Kentucky’s Revenue Cabinet website offers instructions, and information, and is ready to assist taxpayers in navigating the requisition process.

Understanding these key points can make dealing with the Kentucky Tax Requisition form far less daunting, ensuring that taxpayers can navigate their responsibilities with greater confidence and efficiency.

Filling out and using the Kentucky Tax Requisition form requires precise attention to detail and an understanding of the specific needs of the individual or entity submitting the form. Here are several key takeaways to ensure compliance and to maximize efficiency during this process:

Overall, the Kentucky Tax Requisition form is a critical tool for individuals and professionals alike to ensure that they have the necessary documents for tax preparation and filing. Careful completion of this form can facilitate a smoother tax process.

Ky Car Title - This odometer disclosure statement is a requisite for all leased vehicles undergoing a change of ownership in Kentucky.

Emergency Response Plan - Encourages child care facilities to establish written agreements with off-site evacuation locations as a best practice for preparedness.

Kentucky Ui 1 - It includes sections that vary based on the type of employer, such as new businesses or agricultural employers.